The Euro is leaving Greece – and a new Great Depression has entered.

from Merijn Knibbe

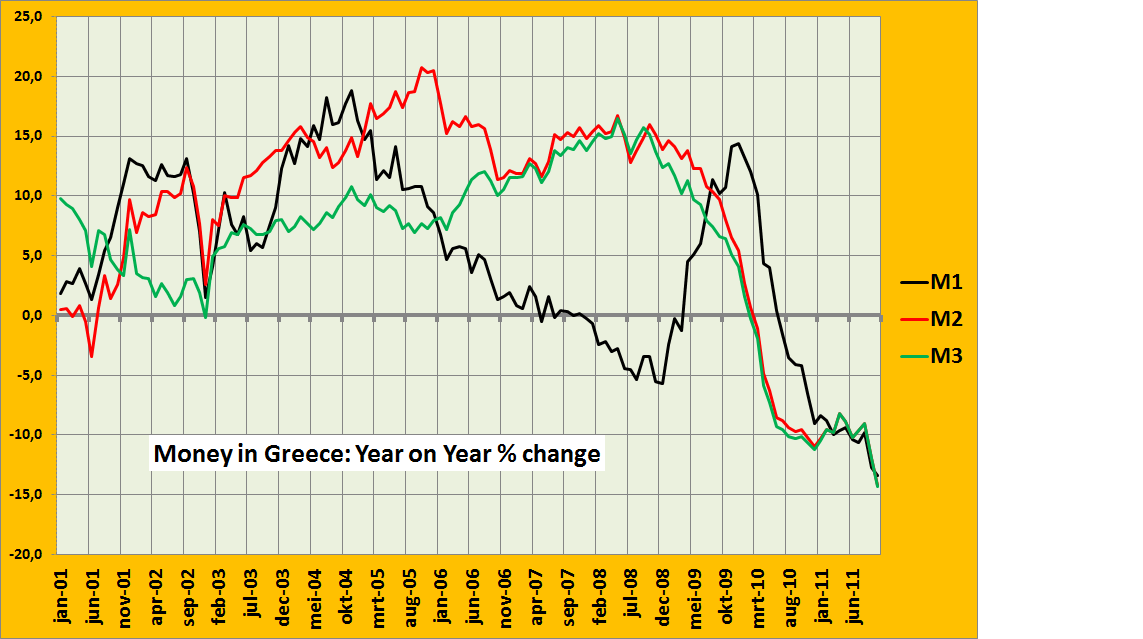

Do Great Depression’ policies lead to ‘Great Depression’ results? Yes, they do. Look at this chart showing the development of the money supply in Greece:

The closest historical precedent is not really ‘Zimbabwe’, but, to the contrary, the Great Depression. There clearly is a ‘bank run’ going on, as stated by Paul de Grauwe. And no, this is not really a ‘Zimbabwe’ – it’s the opposite. Let’s face it, not the government but the country is broke, the present bickering about loans is utter nonsense. The Euro-system has, for whatever reasons, utterly failed. It led to a new Great Depression, in Greece. And yes, we have to look at the increases of the amount of money (read: debts and capital inflows) before 2006, too. But these are not the present problem.

Leave a comment

—– look inside —– $5.94 / $20.00

—– look inside —– $4.90 / $8.00

—– look inside —– $15.99

—– look inside —– $5.99 / 12.99

—– look inside —– $5.93 / $12.99

—– look inside —– $4.97 / $9.90

—— Ugarteche, Puyana and Madi ——

Gerson Lima / Maria Alejandra Madi

Edward Fullbrook and Jamie Morgan

————— Michael Hudson ————–

Maria Alejandra Madi / Jack Reardon

————- Edward Fullbrook ————-

—————— Steve Keen —————–

————— Richard Smith —————

————– Gustavo Marques————

– Victor Beker and Beniamino Moro –

————– Lars Pålsson Syll ————-

—————– Stuart Birks —————-

Edward Fullbrook and Jamie Morgan

———— Armando Ochangco ———-

Shimshon Bichler / Jonathan Nitzan

————— Mauro Gallegati ————–

————— Herman Daly —————-

————— Asad Zaman —————

—————– C. T. Kurien —————

————— Robert Locke —————-

{kind=link}

I would be interested in a more detailed analysis of the above, which I find awfully interesting

Dear Merijn, this is indeed an interesting and worrying for the people of Greece and elsewhere. Two comments: in order to make/hold the statement in the title, it would be interesting/necessary to compare with the Eurozone equivalents… Second, as much as I understand the sentiment to compare with Zimbabwe, it is not suitable. In Zimbabwe, we had astronomic M growth and inflation, with Zimbabwe dollars denominated at trillions (I was there over the whole period of Zimbabwe’s meltdown). Greece is not even close (the opposite direction).

@ Maria, the only detail I can ad is that the amount of cash (part of M-1 money) did increase during the last years, quite bit even…but even then, total M-1 is declining at a double digit rate (i.e. savings deposits and current accounts were declined with about 25 billion euros in two years)

@ Deniz, that second point was exactly the point that I tried to make, I should have made myself clearer. Quite some people still state that expansive monetary policy will lead to a ‘Zimbabwe’ – i.e runaway inflation. But the real problem is that we have to do all we can to fight runaway deflation.

Merijn, I object in principle to the idea of a country going broke. Some of the people within it have gone broke by foolish speculation, and others have made it look broke by taking the nation’s currency elsewhere. These are the ones who should be held responsible. But it does not follow that the Euro – easing trade and reducing brokerage within an economic community large enough to be generously self-supporting – is an utter failure. What has utterly failed is the logic of those who think you have to have EITHER a national currency OR the euro, and lack the imagination to understand the possibilities of having both, with local currencies usable only locally and international traders being made responsible for organising and maintaining their own balance of trade.

Dave,

I think I agree.

Some Georgian MMT: why not introduce a new local (!) land tax, to be paid in New Drachmes, while the local government pays its employees partly in these Drachmes. Market forces will do the rest (oops, the cadastral survey of Greece is still not completed…).

The nasty bit: that we even have to discuss the possibilities you mention, which is why I stick to my statement that ‘The Euro (as a system) has failed’. What has happened in Greece was not only not supposed to happen (of course it wasn’t) but the very possibility was even ruled out.

An example: in hindsight, the Maastricht treaty, more or less the constitution of the Euro-system, should have included rules about deficits AND SURPLUSES on the intra-EZ current accounts (Hat tip: Thomas Colignatus). The one thing Spain and Greece and Ireland and Estonia and Latvia and Lithouania had in common, after 2004, was a very rapidly deteriorating current account (matched, of course, by a surplus in countries like Germany, Austria, the Netherlands, Switzerland and Belgium). Italy is the exception (but Italy also doesn’t have very large government deficits). Remember: deficits in Greece and Latvia were up to 15 and even over 20% of GDP, while even a large economy like the Spanish one had a 10% deficit.

But will the Dutch (surplus of 7% of GDP) and the Germans (5%) agree and actually raise wages?

To Merijn Knibbe

Yes, you are basically right (but countries cant’ go “bankrupt”, that is becoming the “property” of their creditors, they default). The situation is extremly serious in Greece.

We know that the country will have to find 52 billions in 2012 of fresh money.

here are data (from my forthcoming book, alas in French, “Faut-Il Sortir de l’Euro?”, Paris, Le seuil, January 2012) in billions Euros:

A B

Refunding Budget Déficit

2012 31,28 20,65

2013 22,86 16,19

2014 31,32 11,52

2015 19,98 6,61

2016 13,35 6,91

2017 20,83 7,24

2018 9,83 7,57

2019 23,82 7,93

Total 173,27 84,62

Figures for the expected deficit in 2013 and 2014 are largely based on optimistic assumptions, so these data are probably not showing the situation in its full clarity.

Your chart is clearly explaining that there is a move out of the banking system (bank run) but also out of the country.

The haircut promised is to concern only banks and then will not be on 50% of the total debt but much less (probably 32%).

As a result, even with the haircut, Greece is still to have more than 100% of debt to GDP, and will be in such a depression (-5.8% on Y to Y) that the budget deficit is to grow again but this time not because of expenditures but of collapsing budget incomes.

The true dimension of the problem is however to be given by the addition of Greece to Portugal, Spain and Italy.

In Spain the government has already acknowledged that the budget deficit for 2011 is to be 8% GDP and not 6% (as forecated initially). However we are seeing a massive increase in public non-payments (exactly as in Russia between 1995 to 1998). In last December they have reached 133 billions Euros (for a GDP of 1081 Billions). If we assume that around 80 billions are “pure” deficit, then y-the actual deficit for 2011 is to be around 15% of GDP and not 8%. By the way, unemployment has reached the astronomical level of 23% of the work force.

Portugal is too experiencing both a severe GDP contraction and a rise in budget deficit.

Then we have Italy, which is facing the need to refund for 450 billions this year (2012). Even if the government is to run a primary excedent of around 1% GDP, interest on the massive 120% GDP accumulated debt is to rise. Last year they reached 4.6% GDP. But in 2012, with the increase of interest rates (now at 7.12% on ten years bonds), the burden is to be probably 6%, and then the defict at 5%GDP. As the GDP is too contracting now, the debt/GDP ratio is to increase and will probably reach 128% by the end of 2012.

Quite clearly “austerity” policies are showing their limits and I frankly doubt the Eurozone could survive such a crisis.

Jacques SAPIR