Discussing “Can we avoid another financial crisis?”

from WEA Commentaries

My first book since Debunking Economics has just been released in the UK, and will come out in May in the USA. Can we avoid another financial crisis? is a brief (140 page, 25,000 word) explanation for the lay reader of how the 2008 crisis was caused by factors that mainstream economics ignores—fundamentally, the levels of private debt and credit-based demand—and why other countries that avoided a crisis in 2008 are likely to suffer a similar crisis in the near future.

My argument is based in equal measure on my interpretation and model of Hyman Minsky’s Financial Instability Hypothesis (though my book is equation-free), and my analysis of the role of endogenous money—which I now prefer to call “Bank Originated Money and Debt” or BOMD—in causing both economic booms and slumps. The book relies upon the statistical work of the BIS, which since 2014 has started publishing detailed databases on private debt, government debt, house prices, and recently consumer prices. This has made it possible for me to analyse the debt and credit dynamics of 43 countries to identify which have had a crisis, and which are likely to have one in the future.

There are two new insights developed in the book that are new for people who are otherwise familiar with my analysis: that a realistic macroeconomics can be derived directly from macroeconomics itself; and that a rough guide to whether a country is likely to experience a financial crisis can be derived from the BIS data.

Methodology: derive macro from macro

The mainstream is currently undergoing some soul searching about how their models failed both in the crisis and its aftermath, but as usual is convinced that macro should be derived from micro (Blanchard 2016, p. 3). After outlining the complex systems (Anderson 1972) and Neoclassical own-goal critique of this extrapolation fallacy (Sonnenschein 1973, Mantel 1975, Shafer and Sonnenschein 1993), I show that Minsky’s basic insights can be derived directly from basic macroeconomic identities (the employment rate, the wages share of GDP and the private debt to GDP ratio). I don’t show the math in the book, given that this is a book intended to be read by a lay audience, but it’s available on my new website at http://www.profstevekeen.com/crisis/models/.

The Smoking Gun of Credit

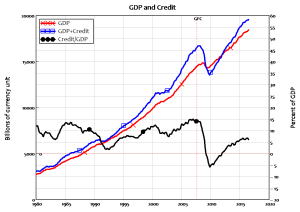

My analysis of the role of credit in aggregate demand and income leads to the proposition that aggregate demand (spent on both goods and assets) is equal to the turnover of existing money plus credit, which is equivalent to the change in private debt (Keen 2015)—see also http://www.profstevekeen.com/crisis/demand/. Since most credit today is used to buy assets rather than goods and services, a rough guide to total monetary demand is given by the sum of GDP plus the annual change in debt (there is double counting of the order of 15% of GDP, but it is still a good guide).

This leads to a chart I describes as “the Smoking Gun of Credit”, which shows how a sharp decline in the rate of growth of private debt when a country’s private debt to GDP ratio is around 150% of GDP is sufficient to cause a serious decline in aggregate demand, income and capital gains.

Figure 1: USA

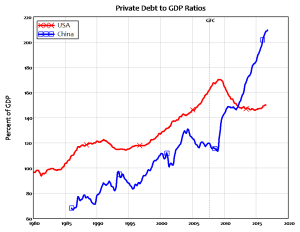

Figure 2: China

The chart explains why the USA had a crisis in 2008 (Figure 1), but countries like China did not (Figure 2): the former suffered a substantial fall in credit-based demand with that demand turning negative for the first time since the Great Depression. China—and several other countries that apparently evaded the worst of the crisis in 2008—managed to stop credit demand from plunging.

But the price of them doing so was an explosion in China’s private debt to GDP ratio, from under 120% of GDP at the time of the GFC to almost 220% as of Q3 2016. The USA, on the other hand, delevered slightly—from 170% to a low of 146%–but is now levering up again.

Figure 3: Comparing China to USA private debt levels

The USA had a crisis in 2008 and is now suffering from “Credit Stagnation” (not “Secular Stagnation”), because with private debt once again exceeding 150% of GDP, it is already in the range where a slowdown in debt growth can cause a recession (see pages 81-83 of the book), and only fractionally below its peak level of private debt).

On the other hand, China’s evasion of the crisis has given it a staggeringly higher debt level, and a dependence on continued demand from credit (the annual change in debt) which is now running at over 25% of GDP. This can’t be sustained (though China can do more than most to switch from credit to government based demand), and China, though by far the largest, is only one of 9-16 countries which evaded the crisis by increased private debt, and now have the pre-requisites for a future crisis of excessive private debt (greater than 150% of GDP) and dependence on unsustainable credit-based demand (exceeding 10% of GDP).

This leads to a natural classification of countries into either the “Walking Dead of Debt” (USA, Europe, UK) or “Zombies to be” (China, Canada, Australia, Korea, Belgium and several others; there are very few that aren’t in one camp or the other—Germany being the notable exception). When these countries’ credit bubbles burst, the global economy will be trapped in not Secular but “Credit Stagnation”.

Finally, I argue for a “Modern Debt Jubilee” as an effective policy to end the crisis, if matched by necessary reforms of bank lending to prevent a future recurrence. Since I believe these policies have a snowflake’s chance in hell of being implemented, my conclusion about the economic future for the planet is rather cynical.

In other news, I have just launched a crowdfunding campaign on Patreon (see https://www.patreon.com/ProfSteveKeen) to enable me to continue my work as a public intellectual.

I see myself as the canary in the coal mine here. Just as non-mainstream, and in particular Post Keynesian economics, is being institutionally recognised (McLeay, Radia et al. 2014) and Neoclassicals are admitting flaws in their paradigm (Blanchard 2016, Kocherlakota 2016, Romer 2016), Neoliberal economic policies applied to Universities in the UK are unwittingly destroying the one toehold that we have in academia—low ranked universities—in a three pronged pincer movement.

The first stage was the introduction of the “Research Excellence Framework” (REF), which focused applications for economics research classification only at the top status universities, where heterodox economics is shunned.

The second was undermining the viability of low status universities via the removal of caps on first year student intakes. High status universities have simply offered more cheap-to-teach humanities vacancies, and high school students, who are utterly uninformed “consumers” of the product called “university”, have taken up these positions.

The third, which may commence next year, is the ranking entire universities as “Gold, Silver or Bronze” teaching institutions in what is known as the “Teaching Excellence Framework” or TEF (the UK seems obsessed with TLAs: “Three Letter Acronyms”). This will surely mean that universities where pluralism is practiced in their economics departments will be ranked as “Bronze” teaching institutions, while high status institutions where the orthodoxy dominates economics tuition will be ranked Silver or Gold.

All these challenges to the viability of low status UK universities has meant that it’s no longer possible for Kingston University to support me in my public role. It’s either take on a full teaching load at Kingston—roughly four times what I’m doing right now—or fund three quarters of my salary. I’ve taken the latter option, and am currently up to US$2800 a month.

Please spread the word about my Patreon campaign. What I’m doing is not a viable option for all heterodox economists of course, but it will give me a public and political platform to challenge both mainstream economics and the deluded Neoliberal approach to university education and research funding.

References

Anderson, P. W. (1972). “More Is Different.” Science177(4047): 393-396.

Blanchard, O. (2016). “Do DSGE Models Have a Future? .” from https://piie.com/system/files/documents/pb16-11.pdf.

Keen, S. (2015). “The Macroeconomics of Endogenous Money: Response to Fiebiger, Palley & Lavoie.” Review of Keynesian Economics3(2): 602 – 611.

Kocherlakota, N. (2016). “Toy Models.” from https://docs.google.com/viewer?a=v&pid=sites&srcid=ZGVmYXVsdGRvbWFpbnxrb2NoZXJsYWtvdGEwMDl8Z3g6MTAyZmIzODcxNGZiOGY4Yg.

Mantel, R. R. (1975). Implications of Microeconomic Theory for Community Excess Demand Functions, Cowles Foundation, Yale University, Cowles Foundation Discussion Papers: 409: 24 pages.

McLeay, M., A. Radia and R. Thomas (2014). “Money creation in the modern economy.” Bank of England Quarterly Bulletin2014 Q1: 14-27.

Romer, P. (2016). The Trouble with Macroeconomics.

Shafer, W. and H. Sonnenschein (1993). Market demand and excess demand functions. Handbook of Mathematical Economics. K. J. Arrow and M. D. Intriligator, Elsevier. 2: 671-693.

Sonnenschein, H. (1973). “Do Walras’ Identity and Continuity Characterize the Class of Community Excess Demand Functions?” Journal of Economic Theory6(4): 345-354.

From: pp.2-4 of WEA Commentaries 7(2), April 2017

http://www.worldeconomicsassociation.org/files/Issue7-2.pdf

Leave a comment

—– look inside —– $5.94 / $20.00

—– look inside —– $4.90 / $8.00

—– look inside —– $15.99

—– look inside —– $5.99 / 12.99

—– look inside —– $5.93 / $12.99

—– look inside —– $4.97 / $9.90

—— Ugarteche, Puyana and Madi ——

Gerson Lima / Maria Alejandra Madi

Edward Fullbrook and Jamie Morgan

————— Michael Hudson ————–

Maria Alejandra Madi / Jack Reardon

————- Edward Fullbrook ————-

—————— Steve Keen —————–

————— Richard Smith —————

————– Gustavo Marques————

– Victor Beker and Beniamino Moro –

————– Lars Pålsson Syll ————-

—————– Stuart Birks —————-

Edward Fullbrook and Jamie Morgan

———— Armando Ochangco ———-

Shimshon Bichler / Jonathan Nitzan

————— Mauro Gallegati ————–

————— Herman Daly —————-

————— Asad Zaman —————

—————– C. T. Kurien —————

————— Robert Locke —————-

Steve, love your writing and your courage to take on this role. I look at this a bit differently. On this blog, I wrote about the invention of money lending and debt. There I said that the first money lenders were always outsiders. This was convenient for two reasons. It allowed the Church’s prohibition on debt and especially usury to continue unchecked. And it allowed debtors to refuse to repay debts but suffer few if any negative repercussions. Monarchs, the principle debtors liked this set up. What would happen today if debtors simply decided for themselves which debts to honor and which not? Would banks and similar organizations cease lending? Would these organizations seek ways to force their debtors to pay? The primary difference in debt now and 500 years ago is that now the banks are not just money lenders. They shape and direct political control and technological development. Meaning that today it’s greatly more difficult to renege on debt than 500 years ago. Is this a good development?

Typical, only for work bound in mainstream paradigm. Leaps in knowledge come from working “outside the box”

Same story, funding controlled by vested interests, which don’t equate to societal interest, and actually hold back progress.

Recognizing the single concept of a new paradigm is the most “outside the box” thing one can experience, and because a new paradigm is simultaneously a new pattern that the single concept fits seamlessly into the thing society can most benefit from.

GFC II?

The Great War only became World War I after World War II. So if there is another GFC, the first will become GFC I and the next will be GFC II. GFC I was predicted, in fact, but noone listened. This time, things could be different.

In any case, GFC II will be an exceptional opportunity for the left in general and non-classical economics in particular. Especially if it’s wider and deeper than GFC I. And that’s why I ask you all what should then be done?

GFC II could happen within two years. Which may not leave time for book publication. So perhaps social media will lead. That depends on us. In any case, we might prepare by discussing possibilities here, including how to make them happen when the time comes.

Maybe the tags are GFC II and 2020 Vision. What do you think?

Excellent question and idea. Here’s a list of ideas and actions I’m confident would help keep us from stumbling into GFC II and WW III.

Preliminaries:

1) Recognize that the paradigm of Debt and Loan Only for the sole form and vehicle for the distribution of credit/money is probably the only socio-economic, financial, political and cultural factor that hasn’t changed in the last 5000 years.

2) Recognize that history shows us that civilizations rarely if ever remedy their disintegration and fall and those that do so on a limited basis address the disintegration via one off debt jubilees and other palliative economic reforms.

3) Recognize that leaders who are unconscious of the above and/or believe it is inevitable like Trump and Bannon may appear to be erudite but are actually conscious or unconscious merchants of chaos AND NOT SAVIORS. Integration is the answer not apathy, “fiddling while Rome burns”, delusionally believing that disintegration is the answer and that god and a coterie of intellectually unastute populist politicians will sort it all out afterward.

4) Recognize that the very process of Wisdom and its fruits of discernment and appropriate and effective action is the integration of only the truths, only the most effective workabilities, only the deepest applicabilities and only highest ethical considerations OF OPPOSING PERSPECTIVES. Wisdom/Integration is the antithesis of orthodoxy. (By the way this process and an actually new and integrative socio-economic, monetary and financial contract is what democrats need to end the disintegrativeness of Trumpism. It has to be starkly and unmistakably better and more beneficial to large constituencies of both parties otherwise it’s onward and downward.)

Actions:

1) All new paradigms are in significant ways conceptually oppositional to old/current ones, thus Monetary Gifting is the new paradigm in opposition to Debt-Burden Only, and monetary, economic and financial policies aligning with the new paradigm are necessary.

2) Policy suggestions that reflect this new paradigm have already been floated before and for some time recently (debt jubilees, UBI, government deficits etc.) and more conscious perception of the natural philosophical concept of the new paradigm (gifting) and the concept behind even it (grace) will give intellectuals the fodder for more integrative ways (recognizing the digital natures of the pricing, monetary and accounting systems) to rapidly implement policies to effect the new paradigm.

3) Take the above insights and social contract policies directly to the individual with social media and a grass roots movement.

4) Broadcast the positive changes resulting from the above to other nations and their business communities and beware any covert or unconscious actions that may make war an easier possibility.

Jonathan and Craig, there are lots of books and plans out there for “remaking” the US economy. Robert Reich makes sensible and doable proposals. Political economist Gar Alperovitz, co-founder of the Democracy Collaborative makes detailed suggestions. Another source is the Institute for New Economic Thinking. The same for PopularResistence.org. All these have the same problems, however. As things stand today, they will never be considered by any American political party, even by Bernie Sanders. Mainstream economists reject these notions. The reasons for rejection? All these proposals reject industrial and financial capitalism in favor of “economic democracy.” Economic decisions would follow the same path as other democratic decisions we make. Or, as activists put it, the economy becomes as it ought to be, “our” economy. This is certainly disruptive and clearly is socialist. As I see it, it’s the only “remaking” that can save both American democracy and the American economy. There are, however sizable segments of the American population not interested in saving either.

Direct and Reciprocal Monetary Distributism is the necessary integration of the sane aspects of capitalism and socialism and a grass roots movement utilizing viral cyber means to communicate its obvious benefits directly to the large constituencies of debt ridden students and recent grads, the dwindling but still enormous middle class and the equally large small to medium sized business community is the fastest route to paradigm change.