Archive

Why Mario Draghi, president of the European Central Bank, is right about monetary financing and debt

Something which I should have done earlier is to check out some publications of Mario Draghi. And I still have to read them. But the ‘blurb’ accompanying them is a pleasant surprise. No Trichet style incredible, ideological nonsense about ergodic systems, confidence fairies and hyper rationality, but this (anno 2004 but an apt description of the Irish case!):

Discussions of the role of derivatives and their risks, as well as discussions of financial risks in general, often fail to distinguish between risks that are taken consciously and ones that are not. To understand the breeding conditions for financial crises, the prime source of concern is not risk per se, but the unintended, or unanticipated accumulation of risks by individuals, institutions or governments including the concealing of risks from stakeholders and overseers of those entities. This report … analyses specific situations in which significant unanticipated and unintended financial risks can accumulate. The focus is, in particular, on the implicit guarantees that governments extend to banks and other financial institutions, and which may result in the accumulation, often unrecognised from the viewpoint of the government, of unanticipated risks in the balance sheet of the public sector … the report shows that a government’s exposure to risk arising from a guarantee is non-linear. For instance, in the case of a government which guarantees the liabilities of the banking system, the additional liability transferred onto the government’s balance sheet by a 10% shock to the capital of firms is larger the lower that capital is to start with. Recognising this non-linearity in the transmission of risk exposures is essential to the reduction of the accumulation of unanticipated risks on the government’s balance sheet. Analyses of recent international financial crises recognise that the implicit guarantees governments extend to banks and corporations create the potential to greatly weaken their balance sheets.

Small wonder that Weidmann gets so angry at Draghi. Draghi is right.

See also this earlier post about the new disequilibrium thinking at the ECB. But they still have to change their targets and start to track GDP inflation instead of just consumer price inflation as well as national debt related variables instead of just Eurozone ‘M-3 money’.

Why Jens Weidmann, president of the Bundesbank, is wrong about monetary financing and debt

According to this speech, Jens Weidmann is obsessed with government deficits as a government deficit might entice politicians to use monetary financing to finance it. But it wasn’t the monetary financing of government deficits which got Europe in trouble. Monetary financing of real estate booms did, in combination with a flawed design of the monetary system, did. Monetary financing of real estate booms led to large deficits on current accounts, increases in private debts which were not matched by increases in wages, house price inflation and, when the bubble burst, house price declines without matching debt relieve. Debts are the largest rigidity in our economy – a flaw in the design of out monetary system.

And we all know the troubles this caused, for instance in Ireland.

Graph 1 shows Irish mortgage debt, comparable graphs can be made for Spain, the Netherlands, the Baltic states etcetera. Monetary financial institutions (MFI’s) have the remarkable prerogative to finance their loans with newly created money, other lenders (like pension funds) have to attract savings first. MFI’s have offloaded a lot of their mortgages to ‘Special Purpose Vehicles’, it is only since June 2010 that the ECB systematically monetary statistics take account of this in a systematical way (which might mean that they underrated pre June 2010 money growth).

Remember: Ireland has only about 4 million inhabitants…

How to re-establish economics as a realist and relevant social science (5 changes)

from Lars Syll

Economics – and especially mainstream neoclassical economics – has as a science lost immensely in terms of status and prestige during the last years. Not the least because of its manifest inability to foresee the latest financial and economic crisis – and its lack of constructive and sustainable policies to take us out of the crisis.

We all know that many activities, relations, processes and events are uncertain and that the data do not unequivocally single out one decision as the only “rational” one. Neither the economist, nor the deciding individual, can fully pre-specify how people will decide when facing uncertainties and ambiguities that are ontological facts of the way the world works.

Neoclassical economists, however, have wanted to use their hammer, and so decided to pretend that the world looks like a nail. Pretending that uncertainty can be reduced to risk and construct models on that assumption have only contributed to financial crises and economic havoc.

How do we put an end to this intellectual cataclysm? How do we re-establish credence and trust in economics? Five changes are absolutely decisive. Read more…

Graphs of the year. Two old ones and two new ones.

I´ve posted some graphs on this blog. Some I especially like:

1. In normal sciences you earn a Nobel price when you estimate or discover something new or enable the measurement of something, like the Higgs particle. Not so in economics. But the ILO, the Bureau of Labor Statistics in the USA and Eurostat deserve the economics ´Nobel´ for defining and estimating ´broad´ U-6 unemployment next to ´normal´ U-3 unemployment. Since about a year, Eurostat publishes estimates this metric of broad unemployment which, among many other things, shows that the situation in Italy is much more dire than indicated by ´normal´ U-3 unemployment. For reasons which I do not understand Eurostat does not publish this graph, so I did it. These data deserve much more attention, in this article I compare the European data with the USA data (p. 152), which is possible because the data are in both cases based upon the ILO definitions.

Graph 1. Broad unemployment in Europe

Latest News

from Peter Radford

Yes it’s hard to focus at this time of year under the best of circumstances. This year is even worse. The background noise provided by the lack of active negotiation over the so-called fiscal cliff, and the Treasury Department’s sudden discovery that we will hit the debt ceiling at year’s end, drown out any day to day news. So in the spirit of giving here’s a look at that humdrum stuff:

House Prices

We learned yesterday, from the Case-Shiller index, that home prices fell in October. Since the index is not seasonally adjusted most people seem to think that this simply reflects the early fall slow down in activity rather than the onset of a prolonged decline. The biggest declines were registered in Chicago – down 1.5% for the month and 1.3% for the last twelve months, and in Boston – down 1.4% for the month, but up 1.4% over the past year. That twelve month decline in Chicago was only one of two city declines: New York was the other where prices dropped 1.3% over the last year.

In general the numbers support the notion of a slow recovery in real estate from a very low level. I doubt prices will accelerate much in 2013, with a lot riding on how income tax rates and deductions are sorted out as part of the current sort-of negotiations in Washington. Read more…

The rise of the robots already happened, household and farming edition

Economists are at the moment discussing the rise of the robots. Yawn. Robots are rising and have done some for some time. The economic discussion about this is a little late. Robotic milking , which enabled dairy farmers to increase the scale of their farm without hiring expensive labour, has been a whopper since about twenty years. And not just the self-employed embrace this technology. I remembered that I once read that there are more household robots than factory robots, a meme which led me to this awesome ´Vacuum cleaners market research´ site with no doubt very good reports like ´Vacuum cleaners in Saudi Arabia´. And with this graph which shows that millions are sold. On Wikipedia one can find a very extensive list of producers (Japan leading the pack). Just like radio in the thirties sales will defy the crisis and households show dynamic adaptions to new technology. Robots changed our life already. Just think of these solar powered lawn mowers! Gadgets like these might help us to cope with the rising number of very old people.

Graph 1. Volume and value of robotic vacuum cleaner sales in the USA and Europe

Why econometrics still hasn’t delivered (wonkish)

from Lars Syll

In the article The Scientific Model of Causality renowned econometrician and Nobe laureate James Heckman writes (emphasis added):

A model is a set of possible counterfactual worlds constructed under some rules. The rules may be laws of physics, the consequences of utility maximization, or the rules governing social interactions … A model is in the mind. As a consequence, causality is in the mind.

Even though this is a standard view among econometricians, it’s – at least from a realist point of view – rather untenable. The reason we as scientists are interested in causality is that it’s a part of the way the world works. We represent the workings of causality in the real world by means of models, but that doesn’t mean that causality isn’t a fact pertaining to relations and structures that exist in the real world. If it was only “in the mind,” most of us couldn’t care less. Read more…

Dutch books and money pumps (wonkish)

from Lars Syll

Neoclassical economics nowadays usually assumes that agents that have to make choices under conditions of uncertainty behave according to Bayesian rules (preferably the ones axiomatized by Ramsey (1931), de Finetti (1937) or Savage (1954)) – that is, they maximize expected utility with respect to some subjective probability measure that is continually updated according to Bayes theorem. If not, they are supposed to be irrational, and ultimately – via some “Dutch book” or “money pump” argument – susceptible to being ruined by some clever “bookie”.

Bayesianism reduces questions of rationality to questions of internal consistency (coherence) of beliefs, but – even granted this questionable reductionism – do rational agents really have to be Bayesian? As I have been arguing elsewhere (e. g. here and here) there is no strong warrant for believing so, but in this post I want to make a point on the informational requirement that the economic ilk of Bayesianism presupposes. Read more…

Graph of the day: Keynes was wrong

A fundamental insight of Keynes was that even in the case of flexible wages and other prices a monetary economy can get stuck in a low-level equilibrium. The developments in Spain, Portugal, Greece and Ireland disprove this idea: if there only was a low-level equilibrium in those countries… The other option is of course that Keynes was basically right but that economic policies aggravated the crisis. Anyway – little could have been done to mitigate the direct consequences of the bursting of the e-nor-mous building housing bubbles in Spain and Ireland. At this moment, however, a kind of secundary crisis has set in, with more job losses in other sectors.

Free trade in Medicare: An alternative to austerity

from Dean Baker

Washington policy debates are chock full of rich people telling poor and middle-class people that they will have to tighten their belts. In fact, in the crazy upside down world of Washington this passes for “courage.”

Cutting back Medicare is one of the favorite forms of belt-tightening being pushed by the elites. Many of the advocates of deficit reduction argue for raising the age of eligibility for Medicare from 65 to 67. Another favorite among this group is to require larger premium payments for Medicare from middle-class beneficiaries. Of course many Republicans would simply privatize Medicare and replace it with a voucher, which almost certainly would not be sufficient to cover the cost of health care.

It is striking in this discussion that no one advocating Medicare cuts ever proposes taking advantage of the lower cost health care systems in other countries. As every policy analyst knows, the problem of Medicare costs stems almost entirely from the fact that our health care system is incredibly inefficient. We pay more than twice as much per person for our health care as people in other wealthy countries even though we have almost nothing to show for it in the way of better health outcomes. Read more…

Oh dear, oh dear, Krugman gets it so wrong, so wrong, on the state of macroeconomics

from Lars Syll

Back in 1938 Keynes wrote in a letter to Harrod:

Economics is a science of thinking in terms of models joined to the art of choosing models which are relevant to the contemporary world. It is compelled to be this, because, unlike the typical natural science, the material to which it is applied is, in too many respects, not homogeneous through time. The object of a model is to segregate the semi-permanent or relatively constant factors from those which are transitory or fluctuating so as to develop a logical way of thinking about the latter, and of understanding the time sequences to which they give rise in particular cases … Good economists are scarce because the gift for using “vigilant observation” to choose good models, although it does not require a highly specialised intellectual technique, appears to be a very rare one.

I came to think of this passage when I read “sort of New Keynesian” economist Paul Krugman’s blog yesterday. Krugman weighs in on the ongoing discussion on the state of macro, arguing that even though he and other “sort of New Keynesian” macroeconomists use the same “equipment” as RBC-New-Classical-freshwater macroeconomists, he resents the allegation that they are a fortiori sharing the the same endeavour. Krugman writes: Read more…

In Greece, history does not rhyme but it repeats itself

From: Sophia Lazaretou (2003), ‘Greek monetary economics in retrospect. The Adventures of the Drachma‘. Bank of Greece working paper no. 2

Starting from 1886, the government relied on large-scale foreign borrowing to finance the budget deficits. During this period the Greek governments were able to raise foreign loans on favourable terms for the implementation of infrastructure projects. After the avoidance of the economic crisis of 1884-85 and the contract of a large foreign loan in 1887 (91 million gold French francs), the country’s credit-worthiness in international money markets was enhanced. From 1889 and onwards, foreign creditors willingly provided the Greek governments with long-term loans with small or no pledges and at a low interest rate. This was because they considered the suspension of the drachma’s convertibility in 1885 as a temporary and extraordinary incident, and expected that the government would soon take anti-inflationary policy measures as it had done in the past. Nevertheless, the high level of primary expenditures and, more importantly, of expenditures for the repayment of the outstanding domestic debt, and their financing through foreign borrowing, created high interest payments, which perpetuated fiscal deficits … In 1890 the country’s reputation as a debtor began to suffer. The impending bankruptcy of Portugal in Europe and of Argentina in Latin America, as well as the crisis of the US dollar, worried foreign creditors who, until then, were generously supplying loans to developing economies without any guarantee and at low interest rates. In December 1893, the government unilaterally suspended payments on servicing the external debt. Foreign creditors demanded the presence of foreign experts for the monitoring of the economic policy pursued and, especially, of the tax collection and management systems. This demand was seen as a pre-condition for the government to pursue a monetary and fiscal policy, which would ensure both the regular repayment of the foreign debt, as well as its repayment in drachmas convertible to gold at par value. After her humiliating defeat in the Greco-Turkish war of 1897 and the resulting huge war indemnity she had to pay to Turkey, Greece was forced to accept the presence of the International Committee for Greek debt management. 1898 was the beginning of a period of intensive disinflation. Successive Finance Ministers curtailed expenditures and increased indirect taxes in an effort to balance the budget. Public confidence in the currency was restored, since private agents knew that the government lacked monetary freedom. Large gold inflows occurred and the drachma came under strong revaluation pressure vis-à-vis the French franc. In 1909, the initial parity of 1:1 was achieved and in March 1910 the drachma joined the gold standard.

Oh Boy: Over the Cliff We Go?

from Peter Radford

No one knows exactly what went on, but this evening’s extraordinary melt down within the House Republican caucus is surely a historical moment.

Here’s the story:

Speaker Boehner has been negotiating a deal to resolve the so-called ‘fiscal cliff’ with President Obama. Set aside whether we think the economy has a debt or budget problem. It certainly has a manufactured fiscal policy problem. The reason the cliff is a rotten thing is that unless it dealt with it will induce a severe contraction in policy staring January 1st. The CBO forecasts a recession if we go over the cliff with GDP dropping by nearly 4.0% in the first quarter. Read more…

Graphs of the day (2). Cashflow and debt in Ireland

In Ireland the cashflow from households to banks is dwindling (graph 1) as less money is available. This led the Irish to restructure their debts cashflows in the sense that less is used to pay down debts and more to prop up interest incomes of banks (graph 2). The cruel paradox: if they pay down more debt and pay less interest the money would disappear ‘into thin air’ (as the banks were allowed to create it by accepting the debts emitted by the households paying down the debts leads to the disappearance of this money). They clearly have to establish a state bank (oops, they have one: the Irish central bank) which buys the bad mortgages at a discount and which has to right to change debt repayments into debt free money which can only be used to pay down government debt or to finance the purchase of the mortgages (sources of the graphs: Irish central bank).

Graph 1. Cash flow problems of Irish households are increasing

Graph 2. Which are ‘solved’ by paying down less debt or even increasing debt as is shown by how bad mortgages are restructured

Help kickstart Minsky

from Steve Keen

As regular readers would know, I have been developing a computer program for building strictly monetary dynamic macroeconomic models. New readers might have seen this article in The Economist:

Reforming macroeconomics: Claudio Borio on the financial cycle

where my work received the following mention:

Steve Keen, an Australian economist, has long argued that macro needs to incorporate these ideas, and has developed a prototype of a computer program, called “Minsky,” that can be used to model economies as monetary systems. So while most economists have not embraced Mr Borio’s agenda for the reformation of macro, some have. That is encouraging news. (Click here for Claudio Borio’s paper)

The program is called Minsky in honor of the late and great monetary economist Hyman Minsky. It is not a model of the economy as such, but a visual tool by which models can be developed.

It has been under development for roughly a year now, thanks to a US$128,000 grant from the Institute for New Economic Thinking. That has enabled me to hire one brilliant programmer, Dr. Russell Standish, for about 10-20 hours a week–the most that a contract programmer can afford to devote to a single project. Consequently, the program as it currently exists represents about 3-4 months of programming time. That’s produced a functional program, but it is still in its infancy. I want to take it to adulthood, and for that I need serious funding that will enable me to hire several top-notch programmers for several years.

That’s where you come in–if you are willing. Next Wednesday I will launch a campaign on Kickstarter to raise development funding for Minsky. Read more…

Graph of the day: global warming is real

A statistically (and according to my experience: historically) very robust rule of thumb to investigate if a time series has an upward or a downward trend is to investigate if minima in one period are higher than maxima in a previous period/if maxima in one period are lower than minima in a previous period. Less robust but still useful: instead of looking at a moving average (or its complicated nephew: a HP-filter) you can look at a line drawn along the maxima or the minima of a series. Applying these methods to the leaked data of the draft of the IPCC’s fifth assessment report yields that the hypothesis that temperatures have been rising fast up to and including 2011 can not be rejected. The Fabius Maximus blog is, using these data, wrong to state that this isn’t the case (but there does seem to be a tendency that differences between maxima and minima are declining).

The Fabius Maximus guys might indeed do well to change their motto: ‘to reignite the spirit of a country grown cold’,

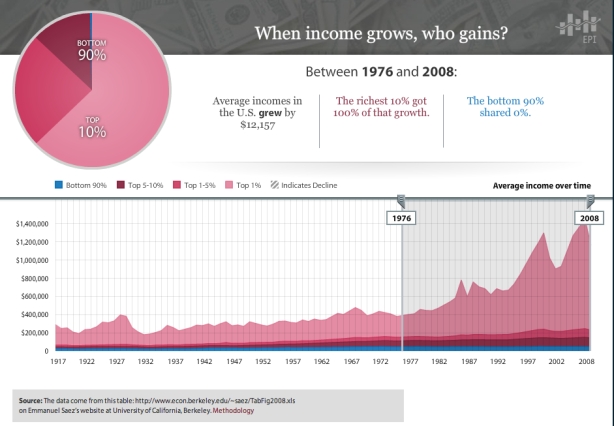

In the USA when income grows, who gains? 1976 – 2008 (chart)

from David Ruccio

That’s right: 100 percent to the top 10 percent and zero for everyone else.

R2 and the crow’s triangular flight

from Lars Syll

In many statistical and econometric studies R2 is used to measure goodness of fit – or more technically, the fraction of variance ”explained” by a regression.

But it’s actually a rather weird measure. As eminent mathematical statistician David Freedman writes: Read more…

For the bottom 60 percent of households in the US, wealth declined from 1983 to 2010 (chart).

How much whipping can democracy take?

from Lars Syll

The 17-nation eurozone has contracted for fourteen straight months. And now it’s not only getting worse in the periphery countries, but also in France and Germany. Unemployment is on the rise everywhere within the eurozone. These are very alarming facts and should be taken seriously.

Richard Koo warns us that the problems – created to a large extent by the euro – may not only endanger our economies, but also our democracy itself:

The question is how long democracy can survive with governments and EU institutions forcing the patient to undergo treatment for the wrong disease. Read more…

—– look inside —– $5.94 / $20.00

—– look inside —– $4.90 / $8.00

—– look inside —– $15.99

—– look inside —– $5.99 / 12.99

—– look inside —– $5.93 / $12.99

—– look inside —– $4.97 / $9.90

—— Ugarteche, Puyana and Madi ——

Gerson Lima / Maria Alejandra Madi

Edward Fullbrook and Jamie Morgan

————— Michael Hudson ————–

Maria Alejandra Madi / Jack Reardon

————- Edward Fullbrook ————-

—————— Steve Keen —————–

————— Richard Smith —————

————– Gustavo Marques————

– Victor Beker and Beniamino Moro –

————– Lars Pålsson Syll ————-

—————– Stuart Birks —————-

Edward Fullbrook and Jamie Morgan

———— Armando Ochangco ———-

Shimshon Bichler / Jonathan Nitzan

————— Mauro Gallegati ————–

————— Herman Daly —————-

————— Asad Zaman —————

—————– C. T. Kurien —————

————— Robert Locke —————-

{kind=link}

Recent Comments