New Greek bailout increases the odds that Grexit will actually happen, despite Washington’s pressure.

from Mark Weisbrot

It is now clear that the European authorities do not intend to let the Greek economy recover any time in the foreseeable future. The primary surpluses that the government has been forced to agree to—2, 3, and 3.5 percent of GDP for the three years of the deal, 2016 through 2018—will not allow Greece to escape its depression, which is now in its sixth year. Even if they miss these targets, which is likely, just trying to do what they have committed to will keep the economy from recovering.

The Foundation for Economic and Industrial Research in Athens has projected that the Greek economy will not recover in 2016. It is worth noting that since 2010 past projections from official sources, e.g., by the IMF, have almost always projected recovery for the following year – even though it never happened until the tiny, short-lived, recovery of 2014.

One can only speculate on the motives for inflicting this harm on the people of Greece. Clearly it is not about the money – the Financial Times estimated that the primary surpluses will contribute about 4.5 billion euros out of what is now an 86 billion euro package. Punishment is probably part of the motivation for these hateful conditions, as well as a fear on the part of the tormentors that “leniency” could encourage people in other vulnerable eurozone economies to vote for left parties or demand an earlier exit from mass unemployment. And the slower the recovery, the more Greece’s creditors—with official creditors (the IMF, ECB, and European governments) now holding 86 percent of the debt—will lose in the debt restructuring that almost everyone now realizes is inevitable. By shutting down the Greek banking system in order to put a gun to Greece’s head before the July 5 referendum, the ECB was sacrificing tens of billions of euros owed to its creditors. And since the financial system is still not back to normal functioning, it means they will lose even more.

The guaranteed extension of depression in Greece certainly changes the equation for Greeks with regard to the costs and benefits of remaining in the eurozone. Polls may still show a majority wanting to stay, but what if the question were put this way?: “By remaining in the eurozone, the Greek economy is likely to experience two or more years of depression. Do you think it is worth this price to keep the euro?” A majority might very well say no.

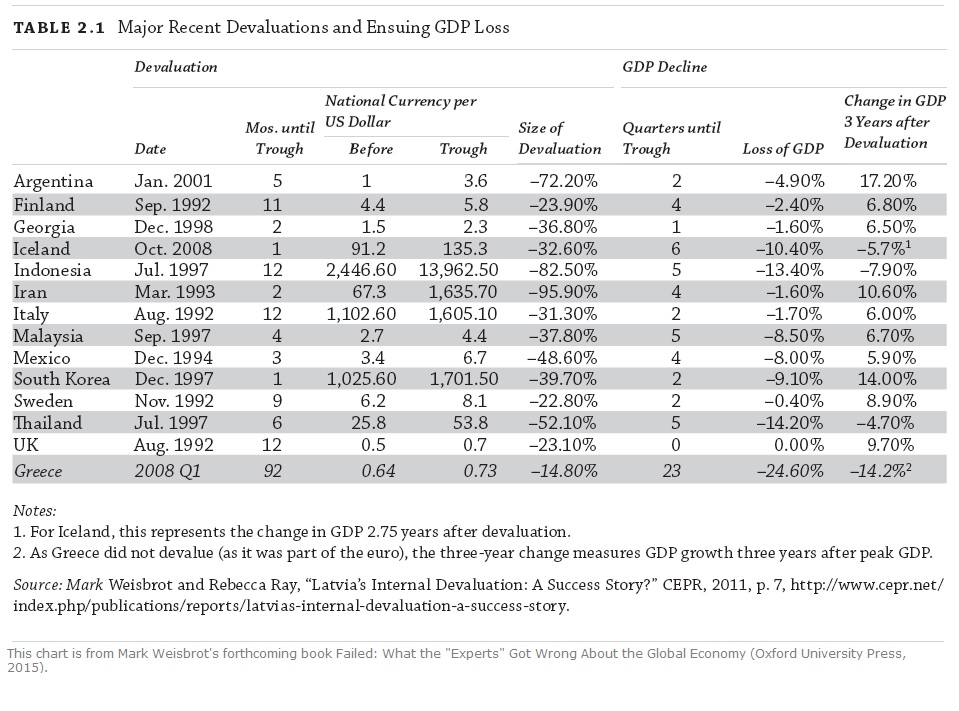

Of course, leaving the euro could be worse than this, but it is very unlikely. A look at financial crises throughout the world over the past two decades shows that Greece has already suffered more damage than nearly any other country. Although the Greek economy would get worse before it got better, given what Greeks are facing under the current program, the end result of leaving would very likely be a faster recovery.

Life after the euro is now being imagined by far more than just euro-skeptics, or economists such as Paul Krugman, who argues that the eurozone countries have never met the conditions for “an optimum currency area.”

Others, including François Hollande of France, are pushing for more fiscal and political integration in order to resolve the problem. But this is very unlikely to help, because it is the politics of the eurozone that are the more immediate and pressing problem. As noted above, this is not about money. The Greek debt problem could have been resolved back in 2010 for a small fraction of the money that creditors have already lost. They have increased their losses enormously by putting Greece through its long depression, and now they are willing to sacrifice even more in order to achieve their political goals. What are those political goals?

Former Greek Finance Minister Yanis Varoufakis, after he left the government, wrote that the German finance minister Wolfgang Schäuble wanted to “put the fear of God into the French and have them accept his model of a disciplinarian eurozone.”

He could have included most of the Eurozone with France, and although Schäuble is the hard-liner, he is not alone in his vision for a new Europe. For direct evidence, we can look at the thousands of pages produced by the “Article IV consultations” that EU countries have regularly with the IMF. These present a clear story of what appears to be an elite consensus, or at least a majority: For the four years 2008 through 2011 (which include the world financial crisis and recession), there is pronounced pattern of recommendations for fiscal tightening, cutting spending, reducing pensions and health care spending, increasing the labor supply and thus reducing the bargaining power of labor, and cutting public employment.

It is for this vision that the European Central Bank, up until September 2012, repeatedly pushed the eurozone to the brink of a financial meltdown, with markets convinced that the existence of the euro itself was at risk. This game of chicken contributed greatly to the additional two years of recession that the eurozone suffered after its initial recovery from the 2009 recession. It was only in July 2012 that Draghi uttered the three words that put an end to the financial crisis, declaring that the ECB would do “whatever it takes” to preserve the euro.

Of course Draghi and the ECB could do the same for Greece as they did for Italy and Spain in 2012, the “too-big-to-fail” debtors whose bond yields were immediately stabilized by his statement, and began a steady decline to very low levels, without the ECB even having to back up its statement with money. But it has chosen instead to do the opposite, to deliberately cause a severe crisis in the Greek financial system, and push it deeper into recession. Apparently they think that Greece is not too big to fail, and that if it ends up out of the euro, the eurozone will persevere. We may well find out in the next year or so, because the Greek people are unlikely to accept the additional suffering that will occur if the current deal is implemented.

Meanwhile, there is another interest here that has been quietly lobbying the European authorities not to push Greece out of the eurozone: the U.S. government. At an IMF board meeting on July 1, the U.S. forced the release of an IMF analysis showing that Greece’s debt was unsustainable. It may have helped Syriza win an overwhelming “no” vote in the July 5 referendum, as the Greek government cited it to prove that their demands for debt relief were reasonable. It was a breach of protocol at the IMF – normally Washington would defer to European wishes on a matter so important to Europe. It was also a shot across the bow, telling the hard-liners especially among the Germans that we (the U.S. government) have our own interests here in not breaking up the eurozone, and we will use our power where necessary and possible to prevent it. Washington does not care about the project for a new, more neoliberal Europe but it does care deeply about the unity of its most important ally – Europe – and has a long and not very proud history of intervention in Greece in order to keep that country within its orbit.

But even Washington’s heavy hand may not be enough to keep Greece within the euro, given the European authorities’ impossible demands. Even debt relief, if the Germans were to concede to it, is almost certainly going to be too little and too late to allow for a Greek economic recovery in the foreseeable future. And without an economic recovery, this deal may very well collapse.

Leave a reply to mike Cancel reply

—– look inside —– $5.94 / $20.00

—– look inside —– $4.90 / $8.00

—– look inside —– $15.99

—– look inside —– $5.99 / 12.99

—– look inside —– $5.93 / $12.99

—– look inside —– $4.97 / $9.90

—— Ugarteche, Puyana and Madi ——

Gerson Lima / Maria Alejandra Madi

Edward Fullbrook and Jamie Morgan

————— Michael Hudson ————–

Maria Alejandra Madi / Jack Reardon

————- Edward Fullbrook ————-

—————— Steve Keen —————–

————— Richard Smith —————

————– Gustavo Marques————

– Victor Beker and Beniamino Moro –

————– Lars Pålsson Syll ————-

—————– Stuart Birks —————-

Edward Fullbrook and Jamie Morgan

———— Armando Ochangco ———-

Shimshon Bichler / Jonathan Nitzan

————— Mauro Gallegati ————–

————— Herman Daly —————-

————— Asad Zaman —————

—————– C. T. Kurien —————

————— Robert Locke —————-

{kind=link}

All the commentaries here on how well Greece would do after exiting the Zone compare it to other nations . . . that have NEVER faced the active animosity of other nations well described here and/or have made clear that they cannot afford for Greece to recover and prove an example to other nations considering exit. Perhaps the Europeans in favor of Grexit would let the Greeks go without further damage, but look at their leadership and ask what makes you think such benevolence would be forthcoming. Those who have been closest to the vitriol directed at the country, that is, the Greek leadership, saw the ire and picked staying in rather than getting out. What makes them wrong?

What makes them wrong is that the people of Greece clearly voted against Tsipras’s foolish snatching of defeat out of the jaws of victory.The point of exiting the Eurozone is that benevolence is not necessary. Just business as usual, and after a short transition, Greece should recover robustly. It takes continual hard work to create depression and misery on the scale of Greece’s. One doesn’t have to speculate with a “Perhaps” – for the negotiations entered Bizarro world – Schauble’s offer of a planned exit was far more favorable to Greece than the continued punishment that Tsipras chose over it.

Active animosity is not really what is important here. The degeneration of basic economic understanding which led to the creation of the Euro is. Just what could “active animosity” do to a Greece outside the EZ? Basically nothing. Greece’s current problems are entirely due to its membership in the Eurozone, and if/when it leaves, an unchanged Eurozone would simply proceed to destroy the economies of the next weaker members.

Weisbrot has far too little skepticism about the reliably unreliable “polls”, which are clearly taking biased samples. Some polls have shown majority support for the drachma over the Euro, but they are generally ignored. Too many outside Greece place unreasonable, excessive trust in polls & pollsters that dramatically miscalled the referendum.

“It is now clear that the European authorities do not intend to let the Greek economy recover any time in the foreseeable future.”

I don’t think so, because what we’re getting at is a core belief of austerity/neoliberalism. They believe austerity works. Obviously those of us on the outside looking into the madhouse think as you do, that surely they must know that running (anti-Keynesian nonsense like) big surpluses during a deep depression means “the Greek economy recover any time in the foreseeable future.”

Devotion to the austerity religion is strong even if irrational, and it is a religion that is very rewarding to a devout follower.