Beyond the trinity formula

from David Ruccio

John Hatgioannides, Marika Karanassou, and Hector Sala are absolutely right: mainstream macroeconomists and policymakers never venture beyond the “holy trinity” of economic growth, inflation, and unemployment.* Everything else, including the distribution of income and wealth, is relegated to the fringes.

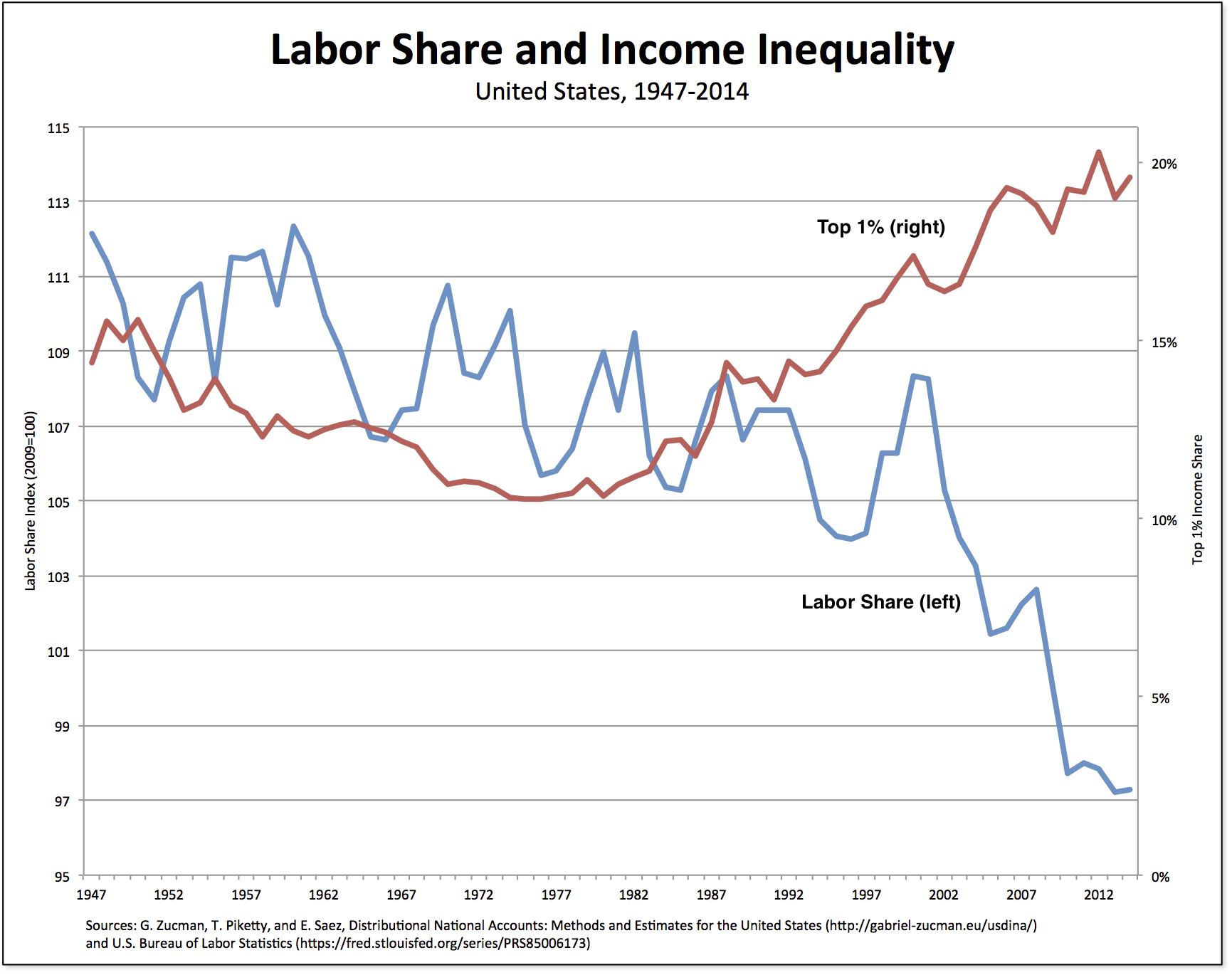

This problem, while always serious, has been magnified in recent decades as inequality has grown to obscene levels, particularly in the United States. The labor share (the blue line in the chart above) has been falling since 1960 and, in the past decade and a half, it dropped an astounding 10.2 percent. Meanwhile, the share of income captured by the top 1 percent (the red line in the chart) has soared, rising from 10.5 percent in 1976 to 19.6 percent in 2014.

In order to rectify the problem, Hatgioannides, Karanassou, and Sala propose to bring inequality in from the margins as the “missing fourth statistic.”

They focus particular attention on inequality in relation to tax contributions. But they do so in the manner that departs from the usual discussion, which leaves the discussion at absolute income tax contributions (such as the share of income taxes paid by each economic group). Those are the numbers we often hear or read, which seek to show how progressive the U.S. tax system is. For example, according to the Tax Foundation, the top 1 percent paid a greater share of individual income taxes (39.5 percent) than the bottom 90 percent combined (29.1 percent).

Instead, Hatgioannides, Karanassou, and Sala concentrate on the ratio of the average income tax per given income group divided by the percentage of national income captured by the same income group (what they call the Effective Income Tax contribution), whence they calculate an inequality index (the Fiscal Inequality Coefficient).

What the Fiscal Inequality Coefficient shows is the relative contribution of filling the fiscal coffers for different pairs of income groups.

In the figure above, they plot the Fiscal Inequality Coefficient based on income shares (they also report a related index based on wealth), of the bottom 90 percent versus the top 10 percent, the bottom 99 percent versus the top 1 percent, and the bottom 99.9 percent versus the top 0.1 percent for 1962, 1980, 1995, 2010, and 2014.

Thus, for example, the Fiscal Inequality Coefficient based on income shares remains relatively constant for all pairs for years 1962 and 1980 but increases significantly by 2010—with the bottom 90 percent effectively contributing 6.5 times more than the top 10 percent, the bottom 99 percent 21.4 times more than the top 1 percent, and the bottom 99.9 percent effectively contributing 89.7 times more than the top 0.1 percent.**

Clearly, the relative income tax burden for those at the top has fallen over time, demonstrating that the U.S. tax system has become less, not more, progressive.

And the authors’ conclusion?

In the current era of fiscal consolidation should the rich be taxed more? Our evidence suggests unequivocally yes.

*Their paper is discussed in the Guardian by Larry Elliott. The submitted version of their article is available here.

**The results are even more dramatic if one calculates the Fiscal Inequality Coefficient based on household wealth shares: in the year 2010, the Bottom 99.9 percent contributed 208.9 times more than the Top 0.1 percent, nearly four times more than what it was in 1980!

Leave a reply to Grayce Cancel reply

—– look inside —– $5.94 / $20.00

—– look inside —– $4.90 / $8.00

—– look inside —– $15.99

—– look inside —– $5.99 / 12.99

—– look inside —– $5.93 / $12.99

—– look inside —– $4.97 / $9.90

—— Ugarteche, Puyana and Madi ——

Gerson Lima / Maria Alejandra Madi

Edward Fullbrook and Jamie Morgan

————— Michael Hudson ————–

Maria Alejandra Madi / Jack Reardon

————- Edward Fullbrook ————-

—————— Steve Keen —————–

————— Richard Smith —————

————– Gustavo Marques————

– Victor Beker and Beniamino Moro –

————– Lars Pålsson Syll ————-

—————– Stuart Birks —————-

Edward Fullbrook and Jamie Morgan

———— Armando Ochangco ———-

Shimshon Bichler / Jonathan Nitzan

————— Mauro Gallegati ————–

————— Herman Daly —————-

————— Asad Zaman —————

—————– C. T. Kurien —————

————— Robert Locke —————-

Transition points around 1980 and again around 1992 seem to indicate times of increase for the top 1%. What key policies changed or were enacted around those times to facilitate the increases? What post-mortem analysis has been done on the impacts of such policies?

The increase for the top 1% came with the financialization of the economy and the insertion of the instruments of financialization into the economic system, e.g., hedge funds, private equity firms, bonus schemes, etc. A lot has been written about the impact of financialization on incomes.

See, my “Financialization, income distribution,and social justice,” rwer, 68, 2014, in which I write:

“Nonetheless, the rise of institutional investors has affected firm governance in two important ways. First, everybody knows that the incomes of the top one percent of Americans, in which category American CEOs belong, have increased dramatically in recent decades. If their percentage of wages is subtracted from labor’s share of seventy-one percent in the late 1970s (the bottom ninety-nine percent of wages earners), the percentage of income of the bottom ninety-nine percent declines as of 2005 by ten percent, which means that only the incomes of the top one percent grew, and did so substantially, in those decades. (Dünhaupt, 10) That the incomes of the richest have benefitted handsomely is common knowledge, but the fact that the growing gap between the top one percent and the bottom ninety-nine percent can be attributed almost exclusively to the financialization of CEO salaries through stock options is perhaps not so well known. Dünhaupt claims as much — that the introduction of stock options into American CEO pay is solely responsible for increasing their share of total incomes from two percent in 2000 to eight percent in 2007 (2011, 19). She concludes that given the proximity of CEOs’ position to capital owners rather than to workers, the stock option is closer to capital income than to wage income and should be classified with the former, i.e., with financialization, rather than with earned wages. Her point has been reinforced during this era of financialization, since the view of labor that prevailed under managerial capitalism as a quasi-fixed asset or human capital changes under financialization to one of “labor being considered a variable cost to be minimized” (Ball & Appelbaum, 6).

Financialization of director salaries encourages those at the top, in their own interest, to adopt a short-term Wall Street focus when running their companies. Mitchell reports that almost eighty percent of more than four hundred chief financial officers in major American corporations recently surveyed, would have at least moderately mutilated their businesses in order to meet analysts’ quarterly profit estimates. Cutting the budgets for research and development, advertising and maintenance and delaying hiring and new projects are some of the long-term harms they would readily inflict on their corporations to achieve good short-term numbers. The same influence of financialization holds when CEOs cut costs by downward pressure on employee wages and the elimination of a firm’s legacy costs (pensions and benefits), policies that have been relentlessly pursued during and since the last two decades of the 20th century (Locke & Spender, 2011, 153-56). These cost-cutting measures fit the financialization view that labor is not a firm asset (human capital) but a variable cost to be minimized. Cutting labor costs has a favorable impact on the market, driving up a firm’s stock price and with it the firm directors’ incomes.

Does anyone know if the trend graphs would look the same for the decline in farmers’ incomes in the 1700’s just before the Revolution (taxing for war), and after (paying cash for war debt)? There were farmers in debtor’s prison who would miss a crop season and then lose the farm. What we know as “Shays; Rebellion” was the farmers’ attempt to close down the local court to delay trials. Some people conclude that the demand in cities for hard cash, regardless of the timing of a crop, was an economic policy against the rural population.

Just to add one other factor to all those factors involved in the increasing inequality of income: the «re-invention» of the world-wide offshore system that has enabled the richer classes to evade/avoid paying progressive personal income taxes and the multinational corporations to evade/avoid paying the corresponding corporate taxes. Hence the relative suspension of the redistribution of wealth function, on the part of the «Welfare» State and the «explosion» of public debt..