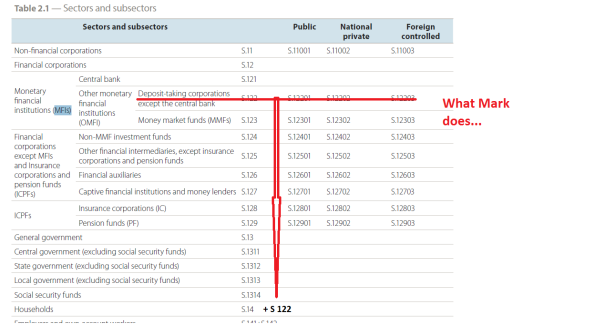

What Mark does. Lack of institutional precision in neoclassical macro leads to an incoherent monetary model

S

Oops. Mark Gertler (with Kiyotaki and Prestipino) does it again: “There has been considerable progress in developing macroeconomic models of banking crises. However, most of this literature focuses on the retail sector where banks obtain deposits from households.” After ‘obtaining’ deposits, these banks are supposed to lend the ‘money’ to households and companies. Source: the 2000+ pages Handbook of [neoclassical, M.K.] Macroeconomics edited by John Taylor. As we know, this is not true. In reality, ‘loans create deposits’. A joint act of lender and borrower, in my 1975 Dutch textbook this was called ‘wederzijdse schuldaanvaarding’ or ‘mutual acceptance of debt’. The lender has a liability towards the borrower (the deposits on the account have to be freely available to the borrower) and the borrower promises to pay back the debt which created these deposits. They can be transmitted from one bank to another. That’s the whole point of the system: in a currency zone bank A accepts deposits created by bank B as means of exchange which at a 1:1 exchange rate can be used to pay down a debt owed by a person to bank A. And the government accepts the deposits at a 1:1 exchange for tax debts. Neat. But these deposits are not somewhere in a vault of a household to a bank. Alas, after about 1980 Anglo-Saxon textbooks started to take over the Dutch market.

Insurance companies and Pension funds obtain deposits (but generally do not lend these but invest them in existing Italian government bonds or other financial assets). What Gertler e.a. in fact do is to assume that the entire money creating banking system (excluding the central bank) is part of the sector households. But in that case, households would be involved in money creating loans to companies. Or the government. Which, in the models, does not seem happen (at least not in an explicit way).

Wouldn’t it be nice and also a hallmark of science if the neoclassical modellers just stuck with the institutional setup of the economy as laid out by the statisticians. My 1975 textbook as consistent with the statistical measurements. Anlo-Saxon textbooks still aren’t – a lack of institutional precision which makes for inconsistent and incoherent models. To take the ‘the map and the territory’ metaphore: yes, a map has to be abstract and I do use a highly abstract map of French highways to get to from my home to the Drome department. But that’s still a map of the territory. I do not use a map of the moon.

Leave a comment

—– look inside —– $5.94 / $20.00

—– look inside —– $4.90 / $8.00

—– look inside —– $15.99

—– look inside —– $5.99 / 12.99

—– look inside —– $5.93 / $12.99

—– look inside —– $4.97 / $9.90

—— Ugarteche, Puyana and Madi ——

Gerson Lima / Maria Alejandra Madi

Edward Fullbrook and Jamie Morgan

————— Michael Hudson ————–

Maria Alejandra Madi / Jack Reardon

————- Edward Fullbrook ————-

—————— Steve Keen —————–

————— Richard Smith —————

————– Gustavo Marques————

– Victor Beker and Beniamino Moro –

————– Lars Pålsson Syll ————-

—————– Stuart Birks —————-

Edward Fullbrook and Jamie Morgan

———— Armando Ochangco ———-

Shimshon Bichler / Jonathan Nitzan

————— Mauro Gallegati ————–

————— Herman Daly —————-

————— Asad Zaman —————

—————– C. T. Kurien —————

————— Robert Locke —————-

So who profits from such misinformation? Are the households then made responsible for all private debt and banks appear never to create any debt themselves? Shame on the banks.

The Anglo-Saxon textbooks used to have it right, having loans create deposits, endogeneous money, wederzijdse schuldaanvaarding and all that, but they went over to the dark side, to nescience somewhat earlier, and this invincible ignorance then spread to Dutch land and elsewhere. Victoria Chick (???, not sure) has a relevant paper.

I recall looking at a textbook of the 50s or 60s that called the incoherent modern economist’s story “the banker’s story” and the loan-creates-deposits story “the economist’s story”. So the dumb bankers needed some edumucating from the smart economists. That’s ok if the economists actually were smarter, as back then. But after the change, it was the other way around. But the economists’ textbooks still insist that they are always the smart guys. :-)