The loanable funds hoax

from Lars Syll

The loanable funds theory is in many regards nothing but an approach where the ruling rate of interest in society is — pure and simple — conceived as nothing else than the price of loans or credits set by banks and determined by supply and demand — as Bertil Ohlin put it — “in the same way as the price of eggs and strawberries on a village market.”

The loanable funds theory is in many regards nothing but an approach where the ruling rate of interest in society is — pure and simple — conceived as nothing else than the price of loans or credits set by banks and determined by supply and demand — as Bertil Ohlin put it — “in the same way as the price of eggs and strawberries on a village market.”

It’s a beautiful fairy tale, but the problem is that banks are not barter institutions that transfer pre-existing loanable funds from depositors to borrowers. Why? Because, in the real world, there simply are no pre-existing loanable funds. Banks create new funds — credit — only if someone has previously got into debt! Banks are monetary institutions, not barter vehicles.

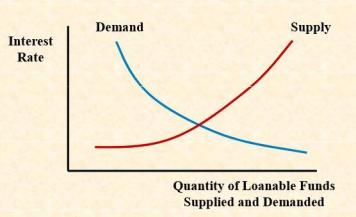

In the traditional loanable funds theory — as presented in mainstream macroeconomics textbooks — the amount of loans and credit available for financing investment is constrained by how much saving is available. Saving is the supply of loanable funds, investment is the demand for loanable funds and assumed to be negatively related to the interest rate. Lowering households’ consumption means increasing savings that via a lower interest.

That view has been shown to have very little to do with reality. It’s nothing but an otherworldly neoclassical fantasy. But there are many other problems as well with the standard presentation and formalization of the loanable funds theory:

1 As already noticed by James Meade decades ago, the causal story told to explicate the accounting identities used gives the picture of “a dog called saving wagged its tail labelled investment.” In Keynes’s view — and later over and over again confirmed by empirical research — it’s not so much the interest rate at which firms can borrow that causally determines the amount of investment undertaken, but rather their internal funds, profit expectations and capacity utilization.

2 As is typical of most mainstream macroeconomic formalizations and models, there is pretty little mention of real world phenomena, like e. g. real money, credit rationing and the existence of multiple interest rates, in the loanable funds theory. Loanable funds theory essentially reduces modern monetary economies to something akin to barter systems — something they definitely are not. As emphasized especially by Minsky, to understand and explain how much investment/loaning/crediting is going on in an economy, it’s much more important to focus on the working of financial markets than staring at accounting identities like S = Y – C – G. The problems we meet on modern markets today have more to do with inadequate financial institutions than with the size of loanable-funds-savings.

3 The loanable funds theory in the ‘New Keynesian’ approach means that the interest rate is endogenized by assuming that Central Banks can (try to) adjust it in response to an eventual output gap. This, of course, is essentially nothing but an assumption of Walras’ law being valid and applicable, and that a fortiori the attainment of equilibrium is secured by the Central Banks’ interest rate adjustments. From a realist Keynes-Minsky point of view this can’t be considered anything else than a belief resting on nothing but sheer hope. [Not to mention that more and more Central Banks actually choose not to follow Taylor-like policy rules.] The age-old belief that Central Banks control the money supply has more an more come to be questioned and replaced by an ‘endogenous’ money view, and I think the same will happen to the view that Central Banks determine “the” rate of interest.

4 A further problem in the traditional loanable funds theory is that it assumes that saving and investment can be treated as independent entities. To Keynes this was seriously wrong:

The classical theory of the rate of interest [the loanable funds theory] seems to suppose that, if the demand curve for capital shifts or if the curve relating the rate of interest to the amounts saved out of a given income shifts or if both these curves shift, the new rate of interest will be given by the point of intersection of the new positions of the two curves. But this is a nonsense theory. For the assumption that income is constant is inconsistent with the assumption that these two curves can shift independently of one another. If either of them shifts, then, in general, income will change; with the result that the whole schematism based on the assumption of a given income breaks down … In truth, the classical theory has not been alive to the relevance of changes in the level of income or to the possibility of the level of income being actually a function of the rate of the investment.

There are always (at least) two parts in an economic transaction. Savers and investors have different liquidity preferences and face different choices — and their interactions usually only take place intermediated by financial institutions. This, importantly, also means that there is no ‘direct and immediate’ automatic interest mechanism at work in modern monetary economies. What this ultimately boils done to is — iter — that what happens at the microeconomic level — both in and out of equilibrium — is not always compatible with the macroeconomic outcome. The fallacy of composition (the ‘atomistic fallacy’ of Keynes) has many faces — loanable funds is one of them.

5 Contrary to the loanable funds theory, finance in the world of Keynes and Minsky precedes investment and saving. Highlighting the loanable funds fallacy, Keynes wrote in “The Process of Capital Formation” (1939):

Increased investment will always be accompanied by increased saving, but it can never be preceded by it. Dishoarding and credit expansion provides not an alternative to increased saving, but a necessary preparation for it. It is the parent, not the twin, of increased saving.

What is ‘forgotten’ in the loanable funds theory, is the insight that finance — in all its different shapes — has its own dimension, and if taken seriously, its effect on an analysis must modify the whole theoretical system and not just be added as an unsystematic appendage. Finance is fundamental to our understanding of modern economies, and acting like the baker’s apprentice who, having forgotten to add yeast to the dough, throws it into the oven afterwards, simply isn’t enough.

All real economic activities nowadays depend on a functioning financial machinery. But institutional arrangements, states of confidence, fundamental uncertainties, asymmetric expectations, the banking system, financial intermediation, loan granting processes, default risks, liquidity constraints, aggregate debt, cash flow fluctuations, etc., etc. — things that play decisive roles in channelling money/savings/credit — are more or less left in the dark in modern formalizations of the loanable funds theory.

It should be emphasized that the equality between savings and investment … will be valid under all circumstances.

In particular, it will be independent of the level of the rate of interest which was customarily considered in economic theory to be the factor equilibrating the demand for and supply of new capital. In the present conception investment, once carried out, automatically provides the savings necessary to finance it. Indeed, in our simplified model, profits in a given period are the direct outcome of capitalists’ consumption and investment in that period. If investment increases by a certain amount, savings out of profits are pro tanto higher …

One important consequence of the above is that the rate of interest cannot be determined by the demand for and supply of new capital because investment ‘finances itself.’

Leave a comment

—– look inside —– $5.94 / $20.00

—– look inside —– $4.90 / $8.00

—– look inside —– $15.99

—– look inside —– $5.99 / 12.99

—– look inside —– $5.93 / $12.99

—– look inside —– $4.97 / $9.90

—— Ugarteche, Puyana and Madi ——

Gerson Lima / Maria Alejandra Madi

Edward Fullbrook and Jamie Morgan

————— Michael Hudson ————–

Maria Alejandra Madi / Jack Reardon

————- Edward Fullbrook ————-

—————— Steve Keen —————–

————— Richard Smith —————

————– Gustavo Marques————

– Victor Beker and Beniamino Moro –

————– Lars Pålsson Syll ————-

—————– Stuart Birks —————-

Edward Fullbrook and Jamie Morgan

———— Armando Ochangco ———-

Shimshon Bichler / Jonathan Nitzan

————— Mauro Gallegati ————–

————— Herman Daly —————-

————— Asad Zaman —————

—————– C. T. Kurien —————

————— Robert Locke —————-

Yes, this troubled me a lot as an undergraduate some 20 years ago until I realized that the average textbook was just complete garbage on monetary economics. Completely scandalous that some people still get taught these fairy tales.

August 12, 2017

I am somewhat surprised that M. Lars Syll did not mention the role of the great Swedish economist Knut Wicksell in the development of the Loanable Funds idealized theory of Money, Savings interest and Investment. I don’t think that that LOANABLE FUNDS was a

deliberate “hoax”.. Unless one wants to designate Wicksell as a deliberate huckster in the same category as the acolytes of the ‘out of Africa’ diktat of human origins: Or, the man-made “global warming cataclysmic-carbon footprint”-I.P.C.C. concoction: Much less by omniscient “illuminati” who exercise diabolic control over the monetary and banking system. Indeed, it can be argued that the very real interventions of modern “dirigiste” states could be just as manipulative and abusive as the bankers and marxoid -fabled “finance capitalists”.

The main lesson to be learned from TELOS & TECHNOS is that a modern quasi-organic interactive economy is a system of evolved emergences cannot be controlled by any imposed diktat of forced redistribution of wealth; No matter how sanctimoniously proclaimed. Or impositions from on-high that treat human economies as ships that can be controlled by algorithmic error-correction. systems.

Please GOOGLE Norman L. Roth, economist

I detect that you are really a very sophisticated algorithm with copious access to Roget’s Thesaurus.

Loanable funds may have been true if/when banks started out as (gold) barter institutions. But even small wild-west American banks soon issued their own dollar notes, becoming monetary institutions quite early. Yes there was a mess of private dollar currencies of uncertain value.

My guess is ‘loanable funds’ is to begin with a faulty explanation of the solvency constraint. Solvency means a bank must have assets (owed to it) at least as high as liabilities. It’s easy to misunderstand the causality or timing of that and make a theory where a bank loans out a supply of assets.

In reality loanable funds is not a constraint, but the supply of assets as loan collateral is. If foreign billionaires put grey money into your bank, and the local housing market can’t support high enough asset prices, you get a bubble and collapse.

«But even small wild-west American banks soon issued their own dollar notes, becoming monetary institutions quite early. Yes there was a mess of private dollar currencies of uncertain value.»

That was called “wildcat banking” and recreating it, but with a government backstop, has been the goal of economic policy since at least the 1994 “Contract on America” by N Gingrich, and probably since the later 1970s.

In effect today’s “money center” megabanks like Citigroup are wildcat banks but the “mess of private dollar currencies of uncertain value” they create are taxpayer-backed. H Minsky wrote already in 1986 in his excellent “Stabilizing an unstable economy: experience and prospects”:

«No matter how exalted a bank may have been, we all know that if assets were marked to market, the net worth of many of the giants of international banking would disappear. Nevertheless these banks are able to sell their liabilities in financial markets, because the buyers believe that they will be protected against losses by the central bank.”

«In reality loanable funds is not a constraint, but the supply of assets as loan collateral is.»

That is better than the “loanable fund” claim, but still not how the financial system today works. What can be used as “collateral” and how much “collateral” is needed is actually a political decision; the major constraint is the regulations that say which collateral and how much the central bank will accept in exchange for lending central bank money at (currently) 0%. The final constraint after that is the acceptability of central bank money to foreign vendors.

Because as MMT says, a central bank can settle any existing debts denominated in central bank money by issuing any required amount of new central bank money, but the central bank can only force domestic vendors to be paid in central bank money, not foreign ones, for any further supplies.

Foreign vendors always ask to be paid on delivery in “hard currency”, whatever they decide is “hard currency”.

I mean real assets in the economy are a constraint on lending. Houses. Not central bank reserves.

When people “put money in the bank” that’s a problem for the bank. The bank can sit on the (clearing system credit) money and make a loss on its operations, or the bank has to find other customers to take equivalent loans. For these loans to have reasonable risk, people must be buying tangible assets, typically houses. If money flows into an economy like Iceland or Ireland, Cyprus, or even London, banks as a whole are motivated to over-value local assets, so they can make loans, so they can profit. When the use-value or sale-value of these assets collapses, or the loans become impossible to service at the economy’s income level, you get a crash.

The limit on banks is not loanable funds. They can crate those by balance sheet operations. The real limit is investible assets.

To the academic economists in the forums, why are fairy tale theories like loanable funds and fractional reserve still in the textbooks?

I know economics is not physics, but physicists have moved phlogiston and aether into the historical failed theories section.

“To the academic economists in the forums, why are fairy tale theories like loanable funds and fractional reserve still in the textbooks?”

Because they are well paid to hold these theories as ‘facts’ .

…” So elaborately has the real nature of this ridiculous proceeding been surrounded with confusion by some of the cleverest and most

skilful advocates the world has ever known, that it still is something of a mystery to ordinary people, who hold their heads and confess they are ” unable to understand finance “. It is not intended that they should.” (Frederick Soddy, The Role Of Money ,1936).

I think you are overly cynical. I think this stays in the books because it is a quite plausible parable, easy to teach (supply and demand curve friendly) and because bad theories reproduce themselves as academics themslves often find it hard to escape from the stuff their own professors taught them. No need for a conspiratorial mindset.

Thank you for your response; however, ” No need for a conspiratorial mindset.” is not a point- When there is empirical evidence that shows how richly rewarded are those who preach “fairy tale theories”;

while those who present possible corrections are called “cranks and thrown to the wolves”.

Just one example-

AFTER more than 80 years-Vindication for the “crank” Frederick Soddy.

https://bestsolutionsfl.wordpress.com/…/after-5000-years-an-answer-yes-virginia-bank..

One wonders just how much government policy is formulated under the loanable funds fallacy. The current rate of interest of the BoE is .25%, mortgages are at least 3% and even peer to peer business lending is between 6 and 9%. Do governments really control the money supply and just what did QE achieve?

«The current rate of interest of the BoE is .25%, mortgages are at least 3% and even peer to peer business lending is between 6 and 9%.»

That is just the obvious point that talk of the interest rate is nonsense, and that some economies are very far from the mythical “zero lower boundary”.

«Do governments really control the money supply»

Depends what you mean by “governments” and “control” and “money”. However that there are wildly different interest rates as you say depending on how politically “relevant” the lender is (insolvent City speculators: 0.25%, tory-voting housing speculators: 3%, productive businesses: 6-9%) seems to show that “governments” are pretty able to target the “money supply” at their best sponsors, by tweaking regulations, accounting standards etc.

«and just what did QE achieve?»

That is a matter of much debate, but as to what it was intended to achieve we have a statement by an ex-member of the Fed Board:

globaleconomicanalysis.blogspot.co.uk/2016/01/former-dallas-fed-governor-richard.html

“What the Fed did, and I was part of that group, we frontloaded a tremendous market rally starting in march of 2009. [ … ] Once again, we frontloaded, at the federal reserve, an enormous rally in order to accomplish a wealth effect.”

” Do governments really control the money supply..” Yes, but they are at the mercy of the banks (Those banks that were given by legislation the right to “print” currency). The banks are not limited by any need for reserves since ‘reserves’ are not required before issuance and are created by issuance-an infinite equation.

This is a ‘fatal flaw’ that will be seen when the amount needed to be made “whole” is so great that the Central Bank will not QE; ergo, “systemic failure”.

EVEN GREENSPAN STATED, “The system is flawed…”

Please, ask again, “To the academic economists in the forums, why are fairy tale theories like loanable funds and fractional reserve still in the textbooks?

Frederick Soddy answered,(The Role Of Money-1936),

… every monetary system must at long last conform, if it is to fulfil its proper role

as the distributive mechanism of society. To allow it to become a source of revenue to private issuers is to create, first, a secret and illicit arm of the government and, last, a rival power strong enough ultimately to overthrow all other forms of government.”

I’m interested in the relevance of bank credit creation to this. Do you think that in an economy with monetary exchange, but with no banks and an exogenous commodity money supply, that the “loanable funds theory” would then hold? Specifically, in such an economy, would changes in investment and savings behaviour simply result in changes in interest rates, as suggested by that diagram or would they, in fact, result in changes in income levels?

Why do modern textbooks still teach nonesense? At least partly because a CLEARLY ARTICULATED alternative, which starts by demolishing existing theories of finance, and provides a coherent and comprehensive alternative currently does not exist, to the best of my knowledge. OF course it is not enough to write the book — one needs to win adherents who would teach it in conventional courses.

Asad, I’m disappointed that, despite my efforts on this and your pedagogy blog, you still don’t seem to grasp that a I do have a clearly articulated alternative, but beauty is in the eye of the beholder. By way of analogy, what may be clearly articulated in arabic may not seem clear to those who know only English. People, economics and theory are all complex, and hoaxes are not possible unless there are plausible alternative interpretations, but modern text books try to achieve clarity by remaining simple. This has the effect of teaching novices to think simple-mindedly: to focus on details rather than seeing details and dynamics in context, and to argue simply for one theory or another rather than seeing how most people taking signs and symbols for reality and interpret the elephant in the room differently. If we are to rewrite the text-books we will need to learn from each other instead of arguing over our short-comings.

In my alternative there are clearly articulated distinctions between (a) an evolutionary context, (b) the role of economics in it, (c) the theory of how economics has changed and (d) how politics carries out economic functions in practice, given (1) how the system is energised, (2) fragmented and usually specialised knowledge and (3) how young or simple-minded leaders predominantly use either the right or the left side of their brain to control their emotions and thus direct their activity. Laughing at Patrick’s glorious vision of Norman as an algorithm attached to Roget’s Thesaurus (both written here in Malvern, incidentally), my view is that one cannot simply reduce an evolving reality to even a nested algorithm (although there is a lot to be learned about the ordering and prioritisation of activity in these). One can, however, draw a topological map (c.f. London Underground) of economic relations and the channels between them (cf. stations and routes). Without it a GDP-type measure of traffic is meaningless, for that doesn’t show us where the monetary traffic comes from, which way round it is going, and the effect alternative paths have in controlling flows in the others.

You are right there has not been alternative – until last year when new textbook, Modern Monetary Theory and Practice: An Introductory Text came out

August 1, 2017

Patrick Newman,

What on earth are you talking about ? Who or where, or what is “Malvern” ?

Perhaps you need to explain to us poor simple minded souls what Rogers Thesaurus has to do with Algorithms. Or tell us what YOU think an Algorithm is. Perhaps you need to be taught the fundamentals of relevance in rational discourse. Please enlighten us.

The same applies to the last two sentences of Mr. Taylor’s contribution. I don’t think either of you understand either the historical /axiomatic context [or the chain of content } of M. Lars Syll’s excellent review of the topic.

Please take my comments only in the didactic sense intended. And…Please read over my letter of August 12, 5:10 P.M. above.

..Please GOOGLE {1} Norman L. Roth {2} Norman L. Roth. Economist {3} Norman L. Roth, Technological Time {4} Norman L. Roth, Current Conception of the Standard of Life

Dear Norman

Jokes are for laughing at, and the joke lies in their irrationality if taken literally. It is better to enjoy them even if they are at your own expense, as when G K Chesterton (a very stout and hairy six foot four) felt he had earned his keep when his hat blew off in the wind and the sight of him chasing it across the common made the local children laugh.

Malvern, the town where I live and worked, is in the West Midlands area of the UK; as I said

– incidentally – both algorithmic programming and Roget’s Thesaurus were developed here.

(Not to mention the circuitry of the world’s first electronically programmed computer and historically the introduction of arabic numbers and the first book in English, he adds proudly).

I saw Patrick as joking about the Turing Test, when you cannot tell whether who you are conversing with is a person or an interactive [advertising?] algorithm in a computer. The Roget’s Thesaurus (a classification of words bringing together those of related meaning) I saw as a reference to your choice of very erudite-sounding words.

As for my “last two sentences”, analogies are intended to make you think. Prof Syll says:

“What is ‘forgotten’ in the loanable funds theory, is the insight that finance — in all its different shapes — has its own dimension, and if taken seriously, its effect on an analysis must modify the whole theoretical system and not just be added as an unsystematic appendage”.

So my theory adds the dimension of time – or more specifically of motion. Whether I’m talking of money or trains I’m talking directed flows rather than quantities or even rates of flow.

Thanks for your commendation of Professor Syll’s “excellent review”. It was certainly worth dwelling on the details.

August 13, 2017

Mr. Taylor,

What do YOUR last two paragraphs mean ? i.e. Who “directs” the “flows” ? The distinction between “stocks” and “flows” in Economic thought, has been well described by many economic thinkers. I suggest you read Nicholas Georgescu-Roegen on the subject, 1971 and 1976 .He wasn’t the only one who contributed to our understanding. And the great French economist, Jean Baptiste Say, introduced the “Circular Flow of Economic Life”, the first overt expression of the static Equilibrium principle . Actually the great Scottish philosopher David Hume made some substantial contributions to our understanding as well.

I know you hate him with a great polemical passion. Possibly for his early description of the now discredited Quantity theory of Money, which devolved into a “reductio ad absurdam” at the hands of Irving -Fisher. If you really believe that “MY theory adds the dimension of time” more specifically, of motion”, I suggest you read the thought of the “Austrian School” of economics about TIME in economics. Unless you “have it in” for them too.

May I humbly suggest that you investigate the concept of TECHNOLOGICAL TIME in Telos & Technos. Chapter Three. Especially on the “Willful Liquidation of Active Time in Neo-Classical Analysis”, Page 5 of the 197 page edition. As for “motion” several of the more “eminent” neoclassical personages opined that economics had its “own laws of motion” similar to astro-physics. The reference is in TELOS & TECHNOS. Maybe you have experienced the same “Eureka” as they did. You’re not in the best company, if that’s the case. I suggest that your notions that economic life can be simulated & ‘guided’ away from error by “navigational” algorithms, is just another version of the neoclassical conceit that economic life can be explained and controlled by emulating a physics metaphor.

You might also investigate the strange phenomenon of “Hydraulic Keynesianism” by one,Tustin, in the 1950s. It’s got lots of stuff about “flows” too. And why don’t you stop invoking the example of the great Claude Shannon as a mentor for your “theory” ? He’s probably turning in his grave at the thought of it. Why don’t you give some thought to how the great Frederick Soddy, the discoverer of Isotopes, trod the primrose path into monetary crankery. But he was not “thrown to the wolves”. He got a well-deserved Nobel prize in Physics for what HE was best at.

Incidently, there’s no such thing as “Arabic numbers”. They were the discovery of the ancient Brahmins. As well as “consciousness”, double-entry book-keeping and the decimal system…Among other things. Check it out for yourself.

Please accept my response in the spirit intended: A Guidance program to “correct” your path away from an erroneous choice of metaphor.

Yours truly,

Norman L. Roth

Dear Norman,

As a mature Christian the word ‘hate’ doesn’t in my thinking apply to people: only to ideas which lead others into diabolical error. Of course people like Macchiavelli, Hume and Hayek have had such ideas, but my passionately drawing attention to this is not ad homenem, but reaction to advocacy and practice of deceit, despite what post-Thatcher moderns since our Orwellian 1984 may subconsciously assume. The work of a few honest and insightful thinkers like Soddy and Shannon is still around, and these I am inclined to respect just as passionately. On flows vs directed motion, the issue is analogous to statistical averaging without reference to standard deviations: okay, one has a circular flow between buyers and sellers via a middle man, but how does that distinguish investment in the not yet produced from that already available to be sold? How can you know my choices of control metaphor are misguided when you clearly haven’t understood that ships and trains can change tracks as well as stick to them?

I’ll look out for Georgescu-Roegen: you are not the only person recommending him. I have seen the Phillips hydraulic model of Keynesianism at Cambridge, but what it emphasises are the knobs that governments and bankers can twiddle, not the difference between money and real goods, hence not the point at issue: access to and investment of the net surplus of real goods. As for my reference to arabic numbers, blame brevity, not lack of understanding. The reference was to their being introduced to Britain by the vicar of Malvern’s Priory Church.

With respect

Dave