Supply and demand deconstructed

from Blair Fix

Prices are caused by supply and demand, right? So say neoclassical economists. If you’ve bought their fairy tale, I recommend you watch this video. In it, Jonathan Nitzan demolishes the neoclassical theory of prices. It’s a master lesson in how to deconstruct a theory.

Here’s the 100-word summary. Nitzan shows that the neoclassical theory of prices fails in six ways:

- Neoclassical theory hinges on utility that cannot be measured

- It relies on demand and supply curves that cannot be observed

- It depends on equilibrium whose existence it cannot confirm

- It requires but cannot show that demand and supply are mutually independent

- It requires but cannot demonstrate that the market demand curve slopes downward

- And it must but cannot measure capital and therefore cannot draw the supply curve, even on paper

So what explains prices?

If neoclassical theory is bunk, then what explains prices? Jonathan Nitzan, together with Shimshon Bichler, argues that prices are inseparable from power.

Here’s a window into Nitzan and Bichler’s thinking. Start with what economists call ‘demand’. If you’re going to buy something you must need or want it. But your want isn’t some fixed property of human nature. It’s a product of your social environment. Want can be massaged, even manufactured. That’s why we have advertising. Everyday, corporations shape our wants so that we buy what they’re selling. This means that demand isn’t some function of autonomous ‘preferences’ (as neoclassical economists would have us believe). Demand is actively shaped by corporate power.

Now let’s look at ‘supply’. It makes sense that if people want something that is scarce, they’ll bid up the price. The problem, though, is that scarcity isn’t just a fact of nature. It’s also an outcome of property rights.

Diamonds, for instance, are a scarce form of carbon. But by itself this scarcity doesn’t explain the price of diamonds. In fact, a primary concern of diamond companies (like De Beers) is that there are too many diamonds. In his seminal PhD thesis, D.T. Cochrane showed that throughout the 20th century, De Beers actively hoarded diamonds to prop up the price. The supply of diamonds was therefore a function power — the power of De Beers to take diamonds off the market.

Administered prices

In capitalist economies, most prices aren’t set by the free market. Instead, prices are administered. They’re set by a manager and then administered to the consumer.

When you stop to think about it, administered pricing is everywhere. Imagine, for instance, walking into Walmart and trying to negotiate prices with the cashier. No one tries to do this because we know it’s foolish. The cashier is powerless to change prices, just as you are powerless to negotiate with Walmart. The reality is that Walmart administers prices to the consumer. So if you want what Walmart is selling, you either pay the listed price or you walk away empty handed.

What’s surprising is not that administered prices exist. Given the power of modern corporations, it would be surprising if prices were not administered. No, what’s surprising is that we’ve known about administered pricing for nearly a century, and yet neoclassical economists still pretend it doesn’t exist. In any other discipline this neglect would be scandalous. But in economics, it’s par for the course. Ignoring contradictory evidence is the tried and true method for maintaining neoclassical dogma.

Let’s have a quick look at this evidence. In the depths of the Great Depression, the economist Gardiner Means was struggling to understand why production had collapsed. According to neoclassical theory, this collapse shouldn’t have happened. Instead, a drop in demand should have been met by a drop in prices. Once supply and demand reached equilibrium, production should have continued unaltered. (Everyone would earn less money, but everything would also cost less. So in ‘real’ terms, nothing would change.) But despite what neoclassical theory predicted, the US was mired in a depression. Why?

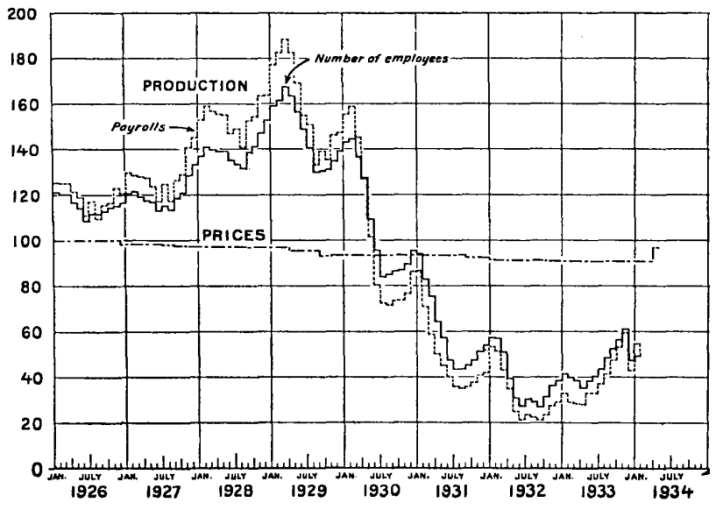

To answer this question, Means turned to the evidence. Looking at the relation between prices and production, he discovered something interesting. In some sectors, prices behaved the way neoclassical theory predicted. Faced with the collapse of consumer spending, firms lowered prices and kept production constant. This was exactly what happened in US agriculture (Figure 1). As the Great Depression hit, agriculture prices collapsed. But production remained virtually unchanged.

If all sectors had behaved like US agriculture, there would have been no Great Depression. But not all sectors behaved this way. In fact, some sectors did exactly what neoclassical theory said they should not do: they kept prices constant and slashed production. Looking at the agricultural implements sector, Means found that when the Great Depression hit, prices hardly changed. Instead, production collapsed (Figure 2).

What explained this behavior? The answer, Means surmised, was that firms in the agriculture implements sector had the power to administer prices. This power meant that when consumer spending collapsed, these firms didn’t cut prices. They cut production. Here’s the take-home message. Gardiner Means discovered that the Great Depression didn’t happen in all sectors of the economy. It happened primarily in sectors with administered pricing.

Means’ work remains a master lesson in how economics should be done. To understand prices (and their relation to production), Means looked at the real world. Sadly, neoclassical economists do the opposite. They proclaim that prices are set by the free market. Then they shrug off contradictory evidence (like Means’) as an ‘exogenous shock’. To paraphrase an old saying, history becomes ‘one damned exogenous shock after another’.1

Administered inflation

Jonathan Nitzan and Shimshon Bichler have continued Gardiner Means’ tradition of studying prices as they are, not as they are imagined (by neoclassical theory). Here’s one of Nitzan and Bichler’s seminal discoveries. Inflation, they find, is largely administered.

On the face of it, this result seems unsurprising. That’s because inflation is usually framed in terms of printing too much money. Since governments control the money printing press, inflation is portrayed as being administered by governments. But this is misleading.

What’s missing from this mainstream description is that inflation is only indirectly about the supply of money. Inflation is directly about the rise of prices. So to understand inflation, you first need to understand how firms set their prices. If prices are administered, it follows that so is inflation. In other words, inflation is created not by printing too much money, but by large firms raising (administered) prices. If this is true, it turns neoclassical theory on its head.

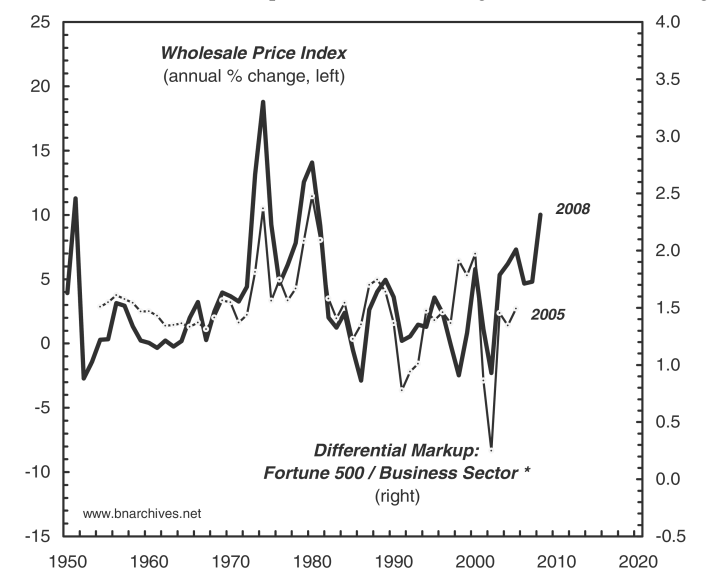

Looking at the evidence, Nitzan and Bichler find that inflation is likely driven by large firms. Figure 3 tells the story. Here Nitzan and Bichler compare the wholesale price index (in the US) to the differential markup of Fortune 500 companies. If you’re not sure what these series mean, I’ll explain shortly. For now, just note that they’re tightly correlated.

Let’s unpack what’s going on. The ‘wholesale price index’ is a measure of inflation. In Figure 3, Nitzan and Bichler plot the rate of change of this index, which indicates how fast prices are rising — the rate of inflation. Nitzan and Bichler then compare this measure of inflation to a measure of profitability known as the ‘markup’. A firm’s markup is its net profit divided by its sales. In Figure 3, Nitzan and Bichler measure the markup of Fortune 500 firms relative to the markup of the whole business sector. They call this the ‘differential markup’.

Fortune 500 firms have markup that is, on average, about 50% greater than other (smaller) firms. This fact is interesting in its own right. But even more interesting is the fluctuation in this differential markup. It moves in lockstep with inflation. In other words, the faster prices rise, the larger the differential markup of Fortune 500 firms. What this means, presumably, is that large firms are able to raise prices faster than small firms. But this implies something shocking: large firms are effectively administering inflation!

Proponents of modern monetary theory (MMT) should take note of this evidence. MMT argues that federal governments don’t have fiscal constraints because they can create their own money. This means that if there is a political will, governments can always finance social spending. A common retort (by MMT opponents) is that printing money will drive inflation. To avoid this specter, governments should balance their budgets (by practicing austerity). Nitzan and Bichler’s evidence provides a strong rebuttal to this argument. Inflation isn’t driven by the government printing press. It’s driven, the evidence suggests, by the pricing practices of large firms. So if you want to avoid inflation, simply regulate prices!

Here’s the take-away message. When we abandon the fairy tale of neoclassical theory, interesting things happen. We start to understand how the world actually works.

Leave a comment

—– look inside —– $5.94 / $20.00

—– look inside —– $4.90 / $8.00

—– look inside —– $15.99

—– look inside —– $5.99 / 12.99

—– look inside —– $5.93 / $12.99

—– look inside —– $4.97 / $9.90

—— Ugarteche, Puyana and Madi ——

Gerson Lima / Maria Alejandra Madi

Edward Fullbrook and Jamie Morgan

————— Michael Hudson ————–

Maria Alejandra Madi / Jack Reardon

————- Edward Fullbrook ————-

—————— Steve Keen —————–

————— Richard Smith —————

————– Gustavo Marques————

– Victor Beker and Beniamino Moro –

————– Lars Pålsson Syll ————-

—————– Stuart Birks —————-

Edward Fullbrook and Jamie Morgan

———— Armando Ochangco ———-

Shimshon Bichler / Jonathan Nitzan

————— Mauro Gallegati ————–

————— Herman Daly —————-

————— Asad Zaman —————

—————– C. T. Kurien —————

————— Robert Locke —————-

Ken, in your comment of 25 August you write

“while economists may not be historians, they still must answer to history. There is no escape from history. People live in history. People make economies. Thus, economies are historical. So, the study of economies must be historical. Also, the methods of social scientists who study economies are historical. Any pretense otherwise merely dooms the study of economies not only to irrelevance but to the attempt to foist falsehoods on non-economists.”

In my comment of 26 august I write

“Ken, if people engaged in economic activity should inform us about the state of the economy, why shouldn’t a study of these people be the source of our knowledge about economics (instead of the gang of theorists we are endlessly discussing).”

It seems that Fix’s article on “the deconstruction of supply and demand economics” and Jonathan Nitsan’s argument justifies this focus on practioneers by emphasizing that prices are inseparable from power” and demand is “actively shaped by corporate power.”

Here we shift from the invisible hand to the “visible hand” that Al Chandler made the focus of his work and that of his school at the Harvard Business School, (see his Pult zer Prize winning 1977 book, and The Visible Hand, and his Scale and Scope, 1990. Chandlers heros are Sloan and General Motors and Dupont, and his long thoroughly researched books about the history of corporate power.

His work and that of so many others I can cite is telling us not to look to economists (Smith,,

Ricardo, etc), to formulate economics but to practitioners and their academic associates when searching for economics, which is what Nitzan and Bischler emphasize.

The criticism that Nitzan presents is no new arguments. Alternative theory of prices has a long history. See Frederic Lee (1998) Post Keynesian Price Theory. The doctrine of administered prices occupies only a quarter of the book. Don’t you know the substantial part of the gang of theorists is already arguing these things endlessly? You must be joking. Or are you intentionally neglecting these facts for the sale of persuading Ken?

Let me add a comment on Blair Fix’s post. Although I do not like Fix’s (or Nitzan’s) “power is everything” theory, he is right to conclude that “When we abandon the fairy tale of neoclassical theory, interesting things happen. We start to understand how the world actually works.” But he is forgetting one important thing. When prices are fixed by suppliers (producers), how the (near) equality of demand and supply is assured in the market economy? Fix gives no hints on this point. The doctrine of administered prices (or more appropriately full-cost pricing) is a half side of the core theory of how modern industrial economy works. We need a theory of quantity adjustment and how adjustment works as a whole (fora an economy as big as a nation or the world). Both sides are explained in our book: Microfoundations of Evolutionary Economics (Prices in Chapter 2 and quantities in Chapter 4). A briefer account is given in my paper: The revival of the classical theory of values (2016).

In our theory, there is no invisible hand. Those who make the economy work are mangers of firms of various ranks (not necessarily top management). If Chandler and other’s advice “not to look to economists” was right when they gave it, it is now wrong. New advice must be “look for good economists”. This is very important in order to prospect the reunification or synthesis of economics and management science.

“If Chandler and other’s advice “not to look to economists” was right when they gave it, it is now wrong. New advice must be “look for good economists”. This is very important in order to prospect the reunification or synthesis of economics and management science.”

Chandler had a big reputation in Japan, especially with the Japanese business historians. I am surprised you don’t seem to know these connections. or maybe it is that Japanese economists don’t pay any more attention to the work of business historians than US economists do.The history of Chandlerianism has evolved a lot since the 1960s. In 2008 the Business History Review had a special issue on Chandler. What has replaced Chandler is the Toyota Kata ane the :ean Production movement.

I believe that Blair and we are aware of alternative price/inflation theories, including Post Keynesian.

See for example “Inflation as Restructuring” (1992) http://bnarchives.yorku.ca/207/.

Maybe the “good economists” are those who pay attention to the firms, the practioneers. When I discovered the Japanese challenge to the Western industrial hegemony in the 1980s and 1990s I looked at the efforts in Germany to meet that challenge. People trained in economics=engineering who had close contacts with firm management best met that challenge. German business economics is firm focused and member of the discipline of economics-engineering carried out the reforms. See my analysis of the Horst Wildemann group at the Munich Technical University, pps. 199ff, The End of Practical man, 1996.

Yoshinriorshi, In the special appraisal of Chandler, summer 2008 issue of he business history review, there is an article that might interest you

Chandler and Business History in Japan

Marie Anchordoguy (a1) Published online by Cambridge University Press: 13 December 2011

Extract

The work and ideas of Alfred D.Chandler Jr. have enriched the field of Japanese business history and our understanding of that nation’s industrial development. Chandler’s studies about the rise of the large, professionally managed, multidivisional firm in the United States highlight factors critical not only to the United States’ capitalist system but also to Japan’s. Indeed, large firms played a dominant role in Japan’s economic takeoff in the late 1800s. As these companies grew, they were transformed into professionally managed corporations. Managers, operating in a clear hierarchical chain of command, built up huge companies, such as Nihon Denki (NEC), Toshiba, Mitsubishi Electric, Hitachi, Nippon Steel, Matsushita, and Toyota. In Japanese as in U.S. firms, the visible hand of management was critical to controlling the flow of work, from the input of raw materials to the production of finished goods.

Strange. I have posted a reply just after Jonathan Nitzan, but it did not appeared.

“Don’t you know the substantial part of the gang of theorists is already arguing these things endlessly? You must be joking.'”

Yoshinori, I wish you knew German, then you would know that German business economists, in their development of a new discipline of business economics, thoroughly discussed administrative pricing, I know because I wrote a book about it, the most important part of which is the chapter: German Business Economics: The Theoretical Achievement, pp. 155-197. The German scientific literature is filled with discussions about costing, management through pricing (Pretiallenkung), transfer pricing, comparative firm performance, etc. I discuss their achievement in this 1984 book. You need to read it at least. The book The End of the Practical Man was published in 1984, then republished in 2006 by Elsevier Science. This is the book that Hartmut Waechter said was the best short treatment of the origins of German business economics in any language.

So do me a favor, read that chapter to discover that neither I nor the German business economists I write about were ignorant of your administrative pricing. The Japanese scholars who studied Betriebswirtwchaftslehre had been learning about it in their seminars in Germany preWWII.

As I stated in my post yesterday, my “Reply” that is posted just after Nitzan was lost, while Robert posted four “Replies” after my first comment. I cannot answer on all points in a Reply. Let me answer slowly in separate “Replies”.

Of course, I know Chandler and his reputation. I had a quick read on Scale and Scope when it was published in Japanese. I had a special interest in this book, because at that time I was much concerned with increasing returns. I wonder if you have correctly read my comment (on August 26, 2020 at 6:24 pm). My comment and his reputation have no connections. I am not denying Chandler’s recommendation. In his time, the recommendation was right. I am saying that economics had changed since then. It is now possible for management scientists and historians to cooperate with some economists. I called them “good economists”.

I have explained in my comment on August 21, 2020 at 2:56 pm to Peter Radford The Missing Middle article why this has become possible, but it seems you have not understood it. I am not surprised with this. For persons who have not considered the question of complexity, it is not easy to understand it. It only means that I must continue to explain it.

I don’t know if you know Professor Takahiro Fujimoto (of Tokyo University). We have two or three co-authored papers and are still collaborating to write a new paper. Fujmoto has books such as Product Development Performance: Strategy, Organization, and Management in the World Auto Industry (with Kim Clark, 1991) and The Evolution of a Manufacturing System at Toyota (1999), to cite only English books. He worked with Kim Clark when he was a graduate student in Havard Business School, but was also a student of Chandler. We are close collaborators in the Japan Association for Evolutionary Economics. The paper The nature of international competition among firms (2019) is a revised version of the paper Inter and Intra Company Competition in the Age of Global Competition (2011-12). The main idea of 2011-12 paper came from Fujimoto and he is the first author. 2019 paper was completely re-written because we had gotten a new theory that explains how the wage rates are determined between nations. As it uses the new theory of international values, I wrote the paper mainly and Fujimoto approved it. I am the first author of the new version.

This is only a small example of collaboration between a management historian (Fujimoto) and an economics theorist (Shiozawa). This kind of examples may not be numerous, but it is now possible because we (I and other colleagues of mine) have a totally different economics than neoclassical economics. Perhaps you have a bad memory of collaborations between economists and historians. In 1960’s a new field of economics emerged in the name of new economic history. You have several times complained about it. It was mainly based in neoclassical economics such as production functions. You must know that our theory refutes production functions. But you may not see the difference, because we use mathematics. It is necessary to continue our discussion. There is a deep groove that separates us.

I collaborated with Chandler on Scale and Scope (part on germany, see his acknowledgementts), so it is a small world. I have just asked Fulbrook to send a copy of German Business Economics: The Theoretical Achievement, to you. I sent it to him. That should make access to this work easier. I am interested in what you are doing, and fully appreciate this refutation of neoclassical economics. At 88, not sure how deeply I can keeep on digging.

I am very familiar with the new economic history, the first chapter, ‘Revionists and Their Theses,’ The End of the Practical Man, is a negative appraisal or the new economic history by me.

A comment on Nitzan and Bichler’s Capital as Power. Routledge, 2009

I have read Chapter 1, the introduction to the whole book Capital as Power by Jonathan Nitzan and Shimshon Bichler. In the first comment of mine on Agust 26, I included Nitzan (in parentheses) among “power is everything” theorists. I have to correct my statement. Nitzan and Bichler are more prudent and thoughtful thinkers. They talk much about Marx and Marxism, but they are not Marxists, at least in the traditional meaning of the words. They are even critical of those politician activists. Here are some phrases I have found in their book.

Nitzan and Bichler want to stay “focused on what drives the capitalists and try to develop a social theory of capitalization that transcends the fetish of material production and capital goods.” (p.14) That is good for themselves. Viewing “capital as power” is a possible aspect of analyses of capitalism. But, I still doubt if this view alone can really explain capitalist accumulation and growth. I believe they need a deeper understanding on how market economy works. They admit lineages of Marx and his followers, Thorstein Veblen, Lewis Mumford and Michal Kalecki. But it is necessary to know that they lack a true foundations of their economics, for example a core framework like our book Microfoundations of Evolutionary Economics.

As Nitzan and Bichler wrote,

Yoshinori Shiozawa:

You write that you “still doubt if this view alone [BN’s] can really explain capitalist accumulation and growth,” and that you believe we “lack a true foundation” and “need a deeper understanding on how market economy works”, like your own.

Doubts are good.

It would be interesting to hear your opinion once you go pass the introduction and read the actual book.

In Management and Higher Education Since 1940 (Cambridge UP, 1989), I quote Peter Lawrence: “when a German manager is asked about the purpose of his enterprise, he never says it is to make money. He is like the Japanese who simply says that profit making is incidental to the greater purpose of the firm, which is to provide a service to its customers, to benefit mankind.”

In my chapter, which I hoped you got, German Business Economics: The Theoretical Achievement (covers 1900-1949), I note that US view, that the firm is a Geldfabrik (a money mill) is known in Germany, most business economists did not accept the view. In Gerrman capitalism, the firm had to serve a greater purpose — all stakeholders, the community — and the duty of business economists was not to measure a firm’s roi (Rentabilitaet) but its efficiency (Wirtschaftlichkeit)

From your problematic’s perspective, the business economists did not accept neoclassical theory of pricing, but the establishing of prices by managers, who administered them to customers. The purpose of German business economics from the beginning was to do that.

In the chapter I sent you, I show, primarily through Eugen Schmallenbach and his Cologne School, how German business economics did just that: with inflation accounting, transfer pricing, costing, management through pricing (Pretiallenkung), uniform accounts, Kontenrahmen that replaced pricing through markets with pricing by administrative managers.

I think success in establishing such a body of business economists is essential to the success of your project.

When I worked in construction laying down sheet metal for roof decks or applying the same type of metal as siding, if there was a slow-down, — e.g. getting a ladder to get to the roof instead of shinnying up the beams because the labour inspector had shown up — the company said that they were “losing money.” Every job we worked seemed to be be “losing money.” What I eventually realized was that they were making less money than they had hoped or expected. So losing money meant not meeting original expectations of profit and having to settle for lower profits.

‘This “equilibrium” graph (Figure 3) and the ideas behind it have been re-iterated so many times in the past half-century that many observes assume they represent one of the few firmly proven facts in economics. Not at all. There is no empirical evidence whatsoever that demand equals supply in any market and that, indeed, markets work in the way this story narrates.

We know this by simply paying attention to the details of the narrative presented. The innocuous assumptions briefly mentioned at the outset are in fact necessary joint conditions in order for the result of equilibrium to be obtained. There are at least eight of these result-critical necessary assumptions: Firstly, all market participants have to have “perfect information”, aware of all existing information (thus not needing lecture rooms, books, television or the internet to gather information in a time-consuming manner; there are no lawyers, consultants or estate agents in the economy). Secondly, there are markets trading everything (and their grandmother). Thirdly, all markets are characterized by millions of small firms that compete fiercely so that there are no profits at all in the corporate sector (and certainly there are no oligopolies or monopolies; computer software is produced by so many firms, one hardly knows what operating system to choose…). Fourthly, prices change all the time, even during the course of each day, to reflect changed circumstances (no labels are to be found on the wares offered in supermarkets as a result, except in LCD-form). Fifthly, there are no transaction costs (it costs no petrol to drive to the supermarket, stock brokers charge no commission, estate agents work for free – actually, don’t exist, due to perfect information!). Sixthly, everyone has an infinite amount of time and lives infinitely long lives. Seventhly, market participants are solely interested in increasing their own material benefit and do not care for others (so there are no babies, human reproduction has stopped – since babies have all died of neglect; this is where the eternal life of the grown-ups helps). Eighthly, nobody can be influenced by others in any way (so trillion-dollar advertising industry does not exist, just like the legal services and estate agent industries).

It is only in this theoretical dreamworld defined by this conflagration of wholly unrealistic assumptions that markets can be expected to clear, delivering equilibrium and rendering prices the important variable in the economy – including the price of money as the key variable in the macroeconomy. This is the origin of the idea that interest rates are the key variable driving the economy: it is the price of money that determines economic outcomes, since quantities fall into place.

But how likely are these assumptions that are needed for equilibrium to pertain? We know that none of them hold. Yet, if we generously assumed, for sake of argument (in good economists’ style), that the probability of each assumption holding true is 55% – i.e. the assumptions are more likely to be true than not – even then we find the mainstream result is elusive: Because all assumptions need to hold at the same time, the probability of obtaining equilibrium in that case is 0.55 to the power of 8 – i.e. less than 1%! In other words, neoclassical economics has demonstrated to us that the circumstances required for equilibrium to occur in any market are so unlikely that we can be sure there is no equilibrium anywhere. Thus we know that markets are rationed, and rationed markets are determined by quantities, not prices.

On our planet earth – as opposed to the very different planet that economists seem to be on – all markets are rationed. In rationed markets a simple rule applies: the short side principle. It says that whichever quantity of demand or supply is smaller (the ‘short side’) will be transacted (it is the only quantity that can be transacted). Meanwhile, the rest will remain unserved, and thus the short side wields power: the power to pick and choose with whom to do business. Examples abound. For instance, when applying for a job, there tend to be more applicants than jobs, resulting in a selection procedure that may involve a number of activities and demands that can only be described as being of a non-market nature (think about how Hollywood actresses are selected), but does not usually include the question: what is the lowest wage you are prepared to work for?

Thus the theoretical dream world of “market equilibrium” allows economists to avoid talking about the reality of pervasive rationing, and with it, power being exerted by the short side in every market. Thus the entire power hiring starlets for Hollywood films, can exploit his power of being able to pick and choose with whom to do business, by extracting ‘non-market benefits’ of all kinds. The pretence of ‘equilibrium’ not only keeps this real power dimension hidden. It also helps to deflect the public discourse onto the politically more convenient alleged role of ‘prices’, such as the price of money, the interest rate. The emphasis on prices then also helps to justify the charging of usury (interest), which until about 300 years ago was illegal in most countries, including throughout Europe.

However, this narrative has suffered an abductio ad absurdum by the long period of near zero interest rates, so that it became obvious that the true monetary policy action takes place in terms of quantities, not the interest rate.

Thus it can be plainly seen today that the most important macroeconomic variable cannot be the price of money. Instead, it is its quantity. Is the quantity of money rationed by the demand or supply side? Asked differently, what is larger – the demand for money or its supply? Since money – and this includes bank money – is so useful, there is always some demand for it by someone. As a result, the short side is always the supply of money and credit. Banks ration credit even at the best of times in order to ensure that borrowers with sensible investment projects stay among the loan applicants – if rates are raised to equilibrate demand and supply, the resulting interest rate would be so high that only speculative projects would remain and banks’ loan portfolios would be too risky.

The banks thus occupy a pivotal role in the economy as they undertake the task of creating and allocating the new purchasing power that is added to the money supply and they decide what projects will get this newly created funding, and what projects will have to be abandoned due to a ‘lack of money’.

It is for this reason that we need the right type of banks that take the right decisions concerning the important question of how much money should be created, for what purpose and given into whose hands. These decisions will reshape the economic landscape within a short time period.

Moreover, it is for this reason that central banks have always monitored bank credit creation and allocation closely and most have intervened directly – if often secretly or ‘informally’ – in order to manage or control bank credit creation. Guidance of bank credit is in fact the only monetary policy tool with a strong track record of preventing asset bubbles and thus avoiding the subsequent banking crises. But credit guidance has always been undertaken in secrecy by central banks, since awareness of its existence and effectiveness gives away the truth that the official central banking narrative is smokescreen.’

https://professorwerner.org/shifting-from-central-planning-to-a-decentralised-economy-do-we-need-central-banks/

Power IS a factor, a major factor in prices, especially in economies where individual income is scarce, i.e. everywhere.

So put the power of commercial survival directly into the individual’s hands with an abundant money-vote and that yet benefits BOTH the individual AND the commercial agent.

Like the dual policies of a 50% discount/rebate at the point of retail sale and at note signing

No?

I am in broad agreement with Blair Fix and Richard A. Werner. However, in the case of Werner’s prescriptions, we must be careful to not flee from the problems of the present by running to the problems of the past. Private and community banking collapses in the past led to economic crises including bank runs and losses of private savings. We do not need to repeat those mistakes.

There is a need for a completely governments owned and government run central bank. With the rejection of monetarism, neoliberalism and austerity, a central bank can be run properly. Money creation is a natural monopoly. Only the central bank, at the orders of the democratic government, should create money. The bureaucrats of the central bank must have all discretion stripped from them. They are there to obey the orders of the democratically elected government. They may give advice but not orders and this within a new MMT-style paradigm.

I see no reason that private banks should ever be permitted the power of direct money creation. They would receive applications from business and private borrowers for loans. These applications (summed in the case of multiple small applications like house mortgagaes) would be submitted. weekly perhaps, to the central bank. The central bank would approve or disapprove the applications according to its government-set criteria. This would include, for example, the need for business loans to be for new production capacity not for asset purchases or speculation. The central bank would charge a rate and set the additional profit mark-up rate permitted to banks.

Beyond all this, there is a clear need for a complete revolution of our society; hopefully a peaceful revolution at the ballot box and then in legislation. The power of large corporations and oligarchic capitalists has to be completely broken. There likely will remain some need for large enterprises. These need to be nationalized where they are natural monopolies. Otherwise, they need to be subjected to break-ups of ownership in an anti-trust fashion. This all gets back to capitalism itself and especially cartel and oligopoly capitalism. These cannot be permitted and MUST be broken up.

Twist any way you like with political economy theory, you cannot in the end avoid the need for a large tranche of command Socialism in the economy. Without it, capitalism continues the concentration of money and power and continues destroying oppressed classes, oppressed nations, the climate and the environment. The evidence is crystal clear. Where capitalism has been most unfettered, the most damage has been done. In the foreseeable future, we need a highly regulated mix of statist or dirigist Socialism and Capitalism as a mixed or hybrid system. However, the capitalism component must be of a small enterprise or large cooperative nature (the latter perhaps like Mondragon).

The power of the capitalists MUST be broken. The power of democratic governance MUST be highly strengthened. The ethical (rights of all) must govern the democratic. The democratic must govern the political economy. The empirical (scientific) must govern the real (what we do to real systems like environment and climates. The political economy must govern economics. Economics is a fifth order discipline (following John Ralston Saul’s insights). Get the other disciplines right and get them to prescribe the economics. We let economics rule society and unleash the disaster of neoliberalism. It’s time to rectify that mistake in a radical and revolutionary fashion. An ideational and voting revolution will be enough unless the capitalists start dishing out reactionary violence (which seems quite likely). If the capitalists start dishing out reactionary violence, they will be opening a door into a very dark future. Soon, the impoverished will vastly outnumber the rich. National strikes, including strikes by data workers, can still shut down everything. A mansion is a cold, cold place if no servants turn up, if no perimeter guards turn up, if no delivery drivers turn up and if data workers implement a data systems shutdown. The masses still have the power. If only they remember it if faced with reactionary violence.

Hear, hear!!!

The power of the current monetary and financial paradigm must be broken or we will remain dominated and de-stabilized by it no matter how much one tries (and fails) to address the excesses and out ethics of capitalism. It IS FINANCE capitalism that we labor within after all.

I agree, after reading key works by Bichler & Nitzan and Fix, that Capital has a manifestation as (social) power. Indeed, the term “capital as power” implies capital as power is just one manifestation of capital. Through my ontological theorizing, I have deduced that financial capital is information. [1] There is no contradiction in saying that capital is information and capital is power. Indeed, there is a necessary complementarity. Financial capital is a notional and formal entity and “clumps” of Financial capital are comprised of a numeric quantity (say 1 million) times a notional dimension (the counter of the numeraire, usually a dollar). In its purest form, Financial capital is information. It is a pattern instantiated in a material or energy medium and it is a pattern capable of influencing or generating other patterns through human agents.

Where living entities, or cells of living agents, are involved as agents, complex patterns which can influence or generate other complex patterns, require a code, a transcriber and/or interpreter of the code and a fabricator of the new complex patterns. We can see this occurring with the operations of RNA and DNA in living cells. In that case, consciousness is not required, so far as we can determine. In the case of human human minds, which have some consciousness but not what would be called absolute extensive consciousness and self-awareness, these minds act as decoders and encoders of the patterns of language information. Mathematics is also a language. The human body is the set of servos which can apply pattern information beyond the body by kinetic means or by language influence. Kinetics is still involved with language as both sound waves and photos transfer energy and information kinetically.

The important point here is the action of the agents, the intelligent human beings, as encoders and decoders of information, who then act on the information in patterns to create other patterns. The information of Financial Capital is a legitimizing and facilitating instruction. It legitimizes and facilitates transfers of labor, materials and energies. Also required are plans (plans for a dam for example) to detail how the labor, materials and energies are to be used. Structural engineers are trained to understand plans and requirements for a dam. But how are all humans as social agents trained to obey the directives of money and capital?

How are all humans as social agents trained to obey the directives of money and capital? This gets to the question of (social) power. It is one thing to be trained in directives. It is another thing to comply. How is compliance generally ensured? This is the point where we discover that mathematics, including the mathematics of economics, is inadequate to give an explanation of the derivation of social power. We have to turn to language. Humans are not natural mathematical calculators. They have to be trained in mathematics. Even humans trained in mathematics and mathematical discipline resort to “ordinary” language or word language when dealing with communications and concepts outside the strict mathematical requirements of their metier or discipline. The more native (perhaps) and solely word- language trained mind is a fuzzy logic machine, not a formal logic or mathematical mind. Its training occurs in actions and words in a largely pre-mathematical milieu. Word language, and thus philosophy in words, containing as they do, nuances and even non-logical contradictions (fuzziness) isare more naturally attuned to explain the phenomena of enculteration and inculcation. Only if we can explain the enculteration and inculcation of money and capital concepts into humans, can we explain the instanitation of social power in monay and capital.

Why do money and capital have (social) power? Training in mathematical literacy cannot alone explain it. That facilitates its technical operations but does not explain its behavioral influence control over people. To explain that we must depart from mathematical theories and return to moral philosophy theories in words which convey nuance and imprecision (the fuzzy logic native to the brain). If Capital does not measure value but instead instantiates (social) power (following Bichler, Nitzan and Fix) then how is that instantiation of social power developed?

Here we need to go to five words useful in this context: words which, with their extensive cultural meanings, cannot be mathematized. These words are gift, bribe, inducement, reward and punishment. These are words of a sociological and behavioral study of economics and are more appropriate tools to discuss what is given to people when they are given or lose money in our system. If money does not measure value how does it instantiate and develop social power operationally? I argue money and capital do this by being one or more of a gift, bribe, inducement, reward or punishment (in negative values). The money system is combined with other systems like the property system and the state violence system to ensure that all capital-appropriate rewards and punishments are delivered. We are trained by gifts, bribes, inducements, rewards and punishments to accede to this system. As a totalizing system it takes control of us. We are servants of the overall notional machine just as we become servants of the physical machines of the system.

The money payed to a day laborer does not value his labor in any way truly equatable to the money values of other things. It simply induces him or her to work. It is an inducement not a valuation. A higher rate to do very difficult or dangerous work is a bribe. The amounts needed to induce or bribe are relative to the precarity of the day laborer’s existence. They are not relative to the “values” of other goods and services in the economic system.

In the end, political economy must be returned to moral philosophy and to democratic and direct action. Words and actions, not mathematics, will be found to be the methods most conformable to the remedying of unjust and unsustainable personal and social empirical realities in a complex, open-ended, emergent, and fuzzy-phenomena world. Reserve mathematics for administration and science. Administration will include administered prices in a setting which ensures the just and equitable meeting of needs, basic and advanced, for every person in society.

Ike, it looks like “supply-and-demand-deconstructed” is a good focus for you! Can I suggest you look at the nature of paradox, and the significance of our reactions to what we sense, i.e. our ability to redirect our senses or our positions or the world around us?

davetaylor1,

I tried to fit too many ideas into too short a post, including ideas which needed to be footnoted. The result was like a free association rave, LOL. I am surprised you got anything coherent out of it.

Your hint about paradox intrigues me. I take very seriously a re-examination of the so-called “Law of noncontradiction”. It’s a principle in logic but I strongly suspect that reality itself does not always obey the “Law of noncontradiction”. It seems to me a sub-set of reality (at the level of the so-called classical laws of science) does obey the Law of noncontradiction, otherwise we would not have been led to derive the law (which I believe has empirical roots). However, our logic works in the “classical” world of classical physics and human physical scale. Such “classical” logic does not necessarily work at the quantum or cosmic scales. Is this what you were referring to?

As to the significance of “our reactions to what we sense”, and “our ability to redirect our senses or our positions or the world around us”. This is also a little vague to me. I’m not sure what you mean by that. From my own position, I suspect that the cultural myths and narratives we tell ourselves and our offspring play a large role in legitimizing our given political economy. Rather than attempting philosophy or political economy one should perhaps attempt new narratives. For example, maybe Charles Dickens played a greater role in developing a social conscience about the plight of the poor than did the moral philosophers.

Ike, your looking at the facts and not other people’s theories of them was not laughable but healthy, and your focus on bribes was both novel here and to the point.

I had hoped you would try to understand for yourself what paradox was, rather than try to understand physical situations in which it has been claimed to apply. Let me point out that it is a phenomenon of classical (whole/part, cause and effect) logic, which ignores time, direction of motion and level of logic (i.e. whether its words are empty symbols or references to variable objects, objects capable of varying other objects (e.g. programs actually available) or objects which actually are varying other things (e.g. active computers). Maths is at the first level, most science at the second, fundamental science at the third and physical reality the fourth.

When the maths leaves out time then you get scientific paradoxes like the chicken and egg or Russell’s paradoxes. These disappear when the chicken egg was that of a pre-chicken, not a chicken, and the barber in the illustration of Russell’s paradox had already shaved himself. The empirical paradox of the sun apparently going round the earth disappears when there is another program capable of producing the result (the earth spinning), but one has to choose the one which makes most sense; likewise with physical creation, where one has to decide between an infinite universe and an infinite creator (a Trinity of states, never-ending because – like those of water – circular). So a black hole sucks in light? Or are we seeing energy coming out, not yet wrinkled enough to be visibly informative?

About changing things, I was being more or less literal. Move your head, and you will change what you see, even if the things around you haven’t changed. Change your position in time, and you will find the (third-level) universal Christian ethic first superseded, then gave way to, a (second-level) pre-Christian moral philosophy of specific types of prohibition. So good for Dickens, choosing to portray reality rather than “law”.